机器学习笔记-逻辑回归实战案例-信用卡欺诈检测

机器学习笔记-逻辑回归实战案例-信用卡欺诈检测

基于creditcard.csv实现数据,建立逻辑回归模型,对数据进行分类

手码不易,点波关注呗

环境:python 3.7.5 and pycharm 2020.1.2

文章目录

- 机器学习笔记-逻辑回归实战案例-信用卡欺诈检测

- 前言

- 一、数据分析与预处理

-

- 数据读取与分析

-

- 1.数据读取与分析

- 2.样本不均衡解决方案

- 样本不均衡解决方法

-

- 标准化

- 特征标准化

- 二、下采样方案

-

- 1.交叉验证

- 2.模型评估方法

-

-

- 3种常见的评估指标

-

- 3.正则化惩罚

- 逻辑回归模型

-

- 1.参数对结果的影响

- 2.混淆矩阵

-

-

- 画一画

-

- 3.分类阈值对结果的影响

- 过采样方法

-

- 1.SMOTE数据生成策略

- 2.过采样应用效果

前言

字数:15871阅读时间:30 mins

提示:以下是本篇文章正文内容,下面案例可供参考

一、数据分析与预处理

数据读取与分析

没有安装模块的先安装模块啦!!

1.数据读取与分析

这是全局的一个模块工具需要,先剧透一波

################数据分析模块导入######################

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.preprocessing import StandardScaler # 导入sklearn标准化模块

from sklearn.model_selection import train_test_split # 数据集合拆分模块

from sklearn.model_selection import KFold

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import recall_score

from sklearn.metrics import confusion_matrix

import itertools

from imblearn.over_sampling import SMOTE

################数据读取######################

data = pd.read_csv('creditcard.csv')

print(data.head(2))

print(data.info())

代码结果:

Time V1 V2 V3 ... V27 V28 Amount Class

0 0.0 -1.359807 -0.072781 2.536347 ... 0.133558 -0.021053 149.62 0

1 0.0 1.191857 0.266151 0.166480 ... -0.008983 0.014724 2.69 0

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 284807 entries, 0 to 284806

Data columns (total 31 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Time 284807 non-null float64

1 V1 284807 non-null float64

2 V2 284807 non-null float64

3 V3 284807 non-null float64

4 V4 284807 non-null float64

5 V5 284807 non-null float64

6 V6 284807 non-null float64

7 V7 284807 non-null float64

8 V8 284807 non-null float64

9 V9 284807 non-null float64

10 V10 284807 non-null float64

11 V11 284807 non-null float64

12 V12 284807 non-null float64

13 V13 284807 non-null float64

14 V14 284807 non-null float64

15 V15 284807 non-null float64

16 V16 284807 non-null float64

17 V17 284807 non-null float64

18 V18 284807 non-null float64

19 V19 284807 non-null float64

20 V20 284807 non-null float64

21 V21 284807 non-null float64

22 V22 284807 non-null float64

23 V23 284807 non-null float64

24 V24 284807 non-null float64

25 V25 284807 non-null float64

26 V26 284807 non-null float64

27 V27 284807 non-null float64

28 V28 284807 non-null float64

29 Amount 284807 non-null float64

30 Class 284807 non-null int64

dtypes: float64(30), int64(1)

memory usage: 67.4 MB

creditcard.csv数据获取,关注博主,传送门

共31列,没有特征解释,显得十分的纯粹。

Amount贷款金额,Class分类结果,其中0表示正常,1表示异常

# 观察正常与异常数据

count_classes = pd.value_counts(data['Class'],sort=True).sort_index()

count_classes.plot(kind = 'bar')

plt.title('Fraud class histogram')

plt.xlabel('Class')

plt.ylabel('Frequency')

plt.show()

通过简单的观察画图,看出正常数据与异常数据的比例大小,是否均衡?

Answers:False

2.样本不均衡解决方案

(1)下采样:通俗讲-假设异常数据500个,正常数据100000个,取正常500个

(2)过采样:通俗讲-假设异常数据500个,正常数据100000个,造999500个异常数据

样本不均衡解决方法

标准化

考虑到Amount数据相对其他数据差异较大,采用特征标准化,公式如下:

![]()

特征标准化

###############数据标准化######################

data['normAmount'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1,1))

data = data.drop(['Time','Amount'],axis=1) # 删除2列

print(data.head(5))

结果展示:

V1 V2 V3 ... V28 Class normAmount

0 -1.359807 -0.072781 2.536347 ... -0.021053 0 0.244964

1 1.191857 0.266151 0.166480 ... 0.014724 0 -0.342475

2 -1.358354 -1.340163 1.773209 ... -0.059752 0 1.160686

3 -0.966272 -0.185226 1.792993 ... 0.061458 0 0.140534

4 -1.158233 0.877737 1.548718 ... 0.215153 0 -0.073403

[5 rows x 30 columns]

正常样本比例: 0.5

异常样本比例: 0.5

下采样总样本数: 984

注意:pandas的reshape一般是传入元组,但是,这里reshape(-1,1)是将心的数据转换成一列

二、下采样方案

##################数据下采样#############

# 目的是获得与异常样本一样多的数据

# 不包含标签的就是特征

x = data.loc[:,data.columns != 'Class']

# 标签

y = data.loc[:,data.columns == 'Class']

number_records_fraud = len(data[data.Class == 1])

# 得到异常样本的索引

fraud_indices = np.array(data[data.Class == 1].index)

# 得到所有正常样本的索引

normal_indices = data[data.Class == 0].index

# https://blog.csdn.net/qq1483661204/article/details/77587881 索引的运用

# 从正常样本中随机抽样指定个数的样本,并取其索引

random_normal_indices = np.random.choice(normal_indices,number_records_fraud,replace=False)

random_normal_indices = np.array(random_normal_indices)

# 有了正常和异常的样本后把他们的索引都拿到手

under_sample_indices = np.concatenate([fraud_indices,random_normal_indices])

# 根据索引得到下采样的所有样本量

under_sample_data = data.iloc[under_sample_indices,:]

x_undersample = under_sample_data.loc[:, under_sample_data.columns !='Class']

y_undersample = under_sample_data.loc[:,under_sample_data.columns == 'Class']

# 打印下采样策略后正负样本比例

print('正常样本比例:',len(under_sample_data[under_sample_data.Class == 0])/len(under_sample_data))

print('异常样本比例:',len(under_sample_data[under_sample_data.Class == 1])/len(under_sample_data))

print('下采样总样本数:',len(under_sample_data))

结果展示:

正常样本比例: 0.5

异常样本比例: 0.5

下采样总样本数: 984

1.交叉验证

什么是交叉验证?

我也显得十分困惑,先看一个图(百度图片)

举个例子:将分出来的测试集,在分为10份,第一次将取9份,留一份作为验证集;第二次,还是取9份,在留其他的一份作为验证集,循环10次。得到10次的计算结果,计算平均数,得到最终模型的评估结果。以上过程,就是交叉验证

###################交叉验证###############################

# 导入数据集切分模块

x_train,x_test,y_train, y_test = train_test_split(x,y,test_size = 0.3,random_state=0)

# 划分数据集,x为特征,y为标签,test_size为测试集比例,random_state设置随机种子

print('原始训练集包含样本数量:',len(x_train))

print('原始测试训练集样本数量:',len(x_test))

print('原始样本样本数量:',len(x_train)+len(x_test))

# 下采样数据集进行划分

x_train_undersample,x_test_undersample,y_train_undersample,y_test_undersample = train_test_split(x_undersample,y_undersample, random_state=0, test_size=0.3)

print('原始训练集包含样本数量:',len(x_train_undersample))

print('原始测试训练集样本数量:',len(x_test_undersample))

print('原始样本样本数量:',len(x_train_undersample)+len(x_test_undersample))

代码结果:

原始训练集包含样本数量: 199364

原始测试训练集样本数量: 85443

原始样本样本数量: 284807

原始训练集包含样本数量: 688

原始测试训练集样本数量: 296

原始样本样本数量: 984

2.模型评估方法

模型评估的真真假假???

百度图片,模糊凑合看

T:True,F:False P:Position N:negative

| 相关(Relevant)正类 | 无关(No-Relevant)负类 | |

|---|---|---|

| 被检索到(Retrieved) | TP:预测正确,判为正类 | FP:预测错误,判为正类 (存伪) |

| 未被检索到(No-Retrieved) | FN:预测错误,判为负类 (去真) | TN:预测正确,判为负类 |

3种常见的评估指标

准确率(accuracy):分类正确的占总的比例

![]()

召回率(recall):分类正确且判为正类占所有正类的比例

![]()

精确度(precision):分类正确占所有判为正类的比例

![]()

3.正则化惩罚

不禁要问:为什么要惩罚呢?

模型拟合有欠拟合、正常拟合、过拟合,过拟合调皮(模型拟合度较高,虽然对训练集比较好,但是一旦实际测试,一塌糊涂),所以要惩罚:

继续问:怎么惩罚呢?

对参数赋予一定权重。常见有L1,L2正则化惩罚项

逻辑回归模型

1.参数对结果的影响

MD,终于开始建模了!

直接上代码,我等不及了!

#################逻辑回归模型######################

def printing_Kflod_scores(x_train_data,y_train_data):

fold = KFold(5,shuffle=False) # len(y_train_data),删除

# 定义不用的正则化惩罚力度

c_param_range = [0.01,0.1,1,10,100]

# 展示结果用的表格

results_table = pd.DataFrame(index = range(len(c_param_range),2),columns=['C_parameter','Mean recall score'])

results_table['C_parameter'] = c_param_range

# k-flod表示K折交叉验证,这里会得到两个索引集合:训练集= indices[0],验证集=indices[1]

j = 0

# 循环遍历不同参数

for c_param in c_param_range:

print('-'*30)

print('正则化惩罚力度:',c_param)

print('-' * 30)

print('')

recall_accs = []

# 分解来执行交叉验证

for iteration,indices in enumerate(fold.split(x_train_data)):

# 指定算法模型,给定参数

lr = LogisticRegression(C=c_param,penalty = 'l1',solver='liblinear')

# 训练模型,主要不要给错索引,训练的一定是训练集,所以x,y的所有都是0

lr.fit(x_train_data.iloc[indices[0],:],y_train_data.iloc[indices[0],:].values.ravel())

# 测试,预测模型效果,用到验证集,索引为1

y_pred_undersample = lr.predict(x_train_data.iloc[indices[1],:].values)

# 预测结果后,进行模型评估,这里用recall_score需要传入预测值和真实值

recall_acc = recall_score(y_train_data.iloc[indices[1],:].values,y_pred_undersample)

# 还要计算平均,先保存结果

recall_accs.append(recall_acc)

print('Iteration',iteration,':召回率 = ',recall_acc)

# 当执行完所有交叉验证后,计算平均结果

results_table.loc[j,'Mean recall score'] = np.mean(recall_accs)

j += 1

print('')

print('平均召回率:',np.mean(recall_accs))

print('')

# 找到参数最好的,也就是recall最高的

best_c = results_table.loc[results_table['Mean recall score'].astype('float32').idxmax()]['C_parameter']

# 打印出最好的结果

print('-'*30)

print('效果最好的模型所选的参数:',best_c)

print('-'*30)

print(results_table)

return best_c

# 函数调用

best_c = printing_Kflod_scores(x_train_undersample,y_train_undersample)

# 在sklearn中惩罚力度,取决于参数C,数值越小,惩罚力度越大。

代码结果:

------------------------------

正则化惩罚力度: 0.01

------------------------------

Iteration 0 :召回率 = 0.9315068493150684

Iteration 1 :召回率 = 0.9178082191780822

Iteration 2 :召回率 = 1.0

Iteration 3 :召回率 = 0.9594594594594594

Iteration 4 :召回率 = 0.9696969696969697

平均召回率: 0.955694299529916

------------------------------

正则化惩罚力度: 0.1

------------------------------

Iteration 0 :召回率 = 0.8493150684931506

Iteration 1 :召回率 = 0.863013698630137

Iteration 2 :召回率 = 0.9491525423728814

Iteration 3 :召回率 = 0.9459459459459459

Iteration 4 :召回率 = 0.8787878787878788

平均召回率: 0.8972430268459988

------------------------------

正则化惩罚力度: 1

------------------------------

Iteration 0 :召回率 = 0.863013698630137

Iteration 1 :召回率 = 0.8904109589041096

Iteration 2 :召回率 = 0.9830508474576272

Iteration 3 :召回率 = 0.9459459459459459

Iteration 4 :召回率 = 0.9090909090909091

平均召回率: 0.9183024720057457

------------------------------

正则化惩罚力度: 10

------------------------------

Iteration 0 :召回率 = 0.863013698630137

Iteration 1 :召回率 = 0.8904109589041096

Iteration 2 :召回率 = 0.9830508474576272

Iteration 3 :召回率 = 0.9324324324324325

Iteration 4 :召回率 = 0.9090909090909091

平均召回率: 0.9155997693030431

------------------------------

正则化惩罚力度: 100

------------------------------

Iteration 0 :召回率 = 0.863013698630137

Iteration 1 :召回率 = 0.8904109589041096

Iteration 2 :召回率 = 0.9830508474576272

Iteration 3 :召回率 = 0.9459459459459459

Iteration 4 :召回率 = 0.9090909090909091

平均召回率: 0.9183024720057457

------------------------------

效果最好的模型所选的参数: 0.01

------------------------------

注意:C=0.01表示正则化力度,随着数值的增加,惩罚力度是减小的。

2.混淆矩阵

混淆矩阵,真头大,简化表述就是:就是TP、FP、FN、TN的统计个数形成的2X2维矩阵

画一画

###############混淆矩阵####################

# 作用:更直观展现结果

def plot_confusion_matrix(cm,classes,title='Confusion Matrix',cmap=plt.cm.Reds):

plt.imshow(cm,interpolation='nearest',cmap = cmap)

plt.title(title)

plt.colorbar()

tick_marks = np.arange(len(classes))

plt.xticks(tick_marks,classes,rotation=0)

plt.yticks(tick_marks,classes)

thresh = cm.max()/2

for i , j in itertools.product(range(cm.shape[0]),range(cm.shape[1])):

plt.text(j,i,cm[i,j],

horizontalalignment='center',

color='white' if cm[i,j] > thresh else 'black')

plt.tight_layout()

plt.ylabel('True label')

plt.xlabel('Predicted label')

# 下采样传值

lr = LogisticRegression(C = best_c,penalty='l1',solver='liblinear')

lr.fit(x_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample = lr.predict(x_test_undersample.values)

# 计算所需的值

cnf_matrix = confusion_matrix(y_test_undersample,y_pred_undersample)

np.set_printoptions(precision=2)

print('召回率:',cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# 绘图

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Confusion matrix')

plt.show()

# 原始数据传值

lr = LogisticRegression(C = best_c,penalty='l1',solver='liblinear')

lr.fit(x_train_undersample,y_train_undersample.values.ravel())

y_pred = lr.predict(x_test.values)

# 计算所需的值

cnf_matrix = confusion_matrix(y_test,y_pred)

np.set_printoptions(precision=2)

print('Recall metric in the testing dataset:',cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

# 绘图

class_names = [0,1]

plt.figure()

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Confusion matrix')

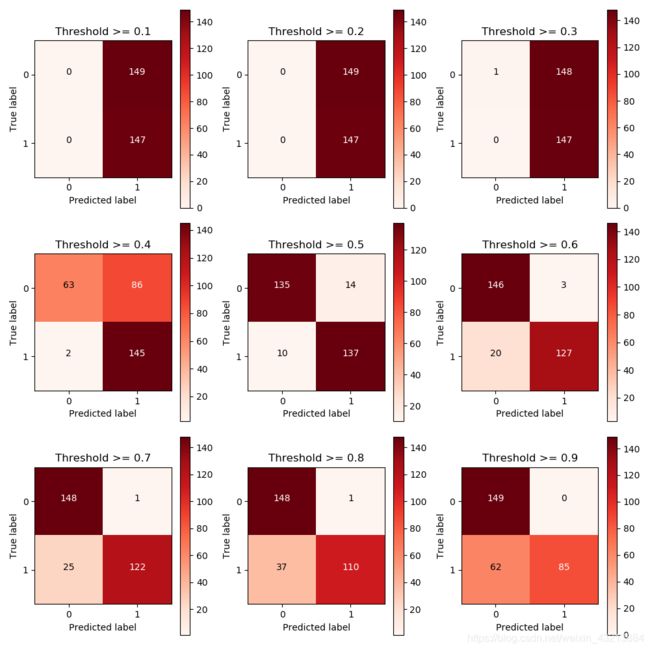

3.分类阈值对结果的影响

分类阈值是个什么东西???

就是把一个样本数据判为一类的概率值,经验是0.5

#####################分类与之对结果的影响########################

# 用之前最好的参数来进行建模

lr = LogisticRegression(C = 0.01,penalty='l1',solver='liblinear')

lr.fit(x_train_undersample,y_train_undersample.values.ravel())

y_pred_undersample_proba = lr.predict_proba(x_test_undersample.values)

# 指定不同的阈值

thresholds = [0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

plt.figure(figsize=(10,10))

j = 1

# 用混淆矩阵来进行展示

for i in thresholds:

# 比较预测概率和给定的阈值

y_test_predictions_high_recall = y_pred_undersample_proba[:,1] > i

plt.subplot(3,3,j)

j += 1

cnf_matrix = confusion_matrix(y_test_undersample,y_test_predictions_high_recall)

np.set_printoptions(precision=2)

print('Recall metric in the testing dataset:',cnf_matrix[1,1]/(cnf_matrix[1,0]+cnf_matrix[1,1]))

class_names = [0,1]

plot_confusion_matrix(cnf_matrix,classes=class_names,title='Threshold >= %s'%i)

Recall metric in the testing dataset: 0.9183673469387755

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 1.0

Recall metric in the testing dataset: 0.9863945578231292

Recall metric in the testing dataset: 0.9319727891156463

Recall metric in the testing dataset: 0.8639455782312925

Recall metric in the testing dataset: 0.8299319727891157

Recall metric in the testing dataset: 0.7482993197278912

Recall metric in the testing dataset: 0.5782312925170068

当阈值在0.5时,召回率偏高,误判样本也明显较多。

当阈值在0.6时,召回率有所下降,误判样本也明显减少。

选谁呢?诶!根据业务需求!

过采样方法

1.SMOTE数据生成策略

为什么要SMOTE,我们看前面的结果,虽然召回率较高,但是误判的样本也不少

大概思路:

对每一个异常样本,首先找到(欧氏距离)最近的同类样本,然后在他们之间的举例之上取0-1中的一个随机小数作为比例,在加到原始数据点,就得到最新的异常样本。

2.过采样应用效果

#############SMOTE数据生成策略###############

# pip install imblearn

features_train, features_test, labels_train, labels_test = train_test_split(x,

y,

test_size=0.3,

random_state=0)

oversampler = SMOTE(random_state=0)

os_features,os_labels = oversampler.fit_sample(features_train,labels_train)

os_features = pd.DataFrame(os_features)

os_labels = pd.DataFrame(os_labels)

best_c = printing_Kflod_scores(os_features,os_labels)

lr = LogisticRegression(C = best_c,penalty='l1',solver='liblinear')

lr.fit(os_features,os_labels.values.ravel())

y_pred = lr.predict(features_test.values)

# 计算混淆矩阵

cnf_matrix = confusion_matrix(labels_test,y_pred)

np.set_printoptions(precision=2)

print('Recall metric in the testing dataset:', cnf_matrix[1, 1] / (cnf_matrix[1, 0] + cnf_matrix[1, 1]))

class_names = [0, 1]

plt.figure()

plot_confusion_matrix(cnf_matrix, classes=class_names, title='Confusion matrix')

plt.show()

结果展示:

------------------------------

正则化惩罚力度: 0.01

------------------------------

Iteration 0 :召回率 = 0.9285714285714286

Iteration 1 :召回率 = 0.912

Iteration 2 :召回率 = 0.9129742033383915

Iteration 3 :召回率 = 0.897245217129147

Iteration 4 :召回率 = 0.8974336427701082

平均召回率: 0.9096448983618151

------------------------------

正则化惩罚力度: 0.1

------------------------------

Iteration 0 :召回率 = 0.9285714285714286

Iteration 1 :召回率 = 0.92

Iteration 2 :召回率 = 0.9145169448659585

Iteration 3 :召回率 = 0.8985139497782858

Iteration 4 :召回率 = 0.8987777456756315

平均召回率: 0.9120760137782609

------------------------------

正则化惩罚力度: 1

------------------------------

Iteration 0 :召回率 = 0.9285714285714286

Iteration 1 :召回率 = 0.92

Iteration 2 :召回率 = 0.914693980778958

Iteration 3 :召回率 = 0.8988028690944264

Iteration 4 :召回率 = 0.8990917884105669

平均召回率: 0.9122320133710762

------------------------------

正则化惩罚力度: 10

------------------------------

Iteration 0 :召回率 = 0.9285714285714286

Iteration 1 :召回率 = 0.92

Iteration 2 :召回率 = 0.914693980778958

Iteration 3 :召回率 = 0.8991294735387592

Iteration 4 :召回率 = 0.8991169118293617

平均召回率: 0.9123023589437016

------------------------------

正则化惩罚力度: 100

------------------------------

Iteration 0 :召回率 = 0.9285714285714286

Iteration 1 :召回率 = 0.92

Iteration 2 :召回率 = 0.9146686899342438

Iteration 3 :召回率 = 0.8990917884105669

Iteration 4 :召回率 = 0.8991169118293617

平均召回率: 0.9122897637491203

------------------------------

效果最好的模型所选的参数: 10.0

------------------------------

C_parameter Mean recall score

0 0.01 0.909645

1 0.10 0.912076

2 1.00 0.912232

3 10.00 0.912302

4 100.00 0.91229

Recall metric in the testing dataset: 0.9183673469387755

Process finished with exit code 0