学习笔记31-自回归-建立时间序列预测模型(ARIMA方法)

时间序列(Time Series)定义: 按照时间的顺序把一个随机事件变化发展的过程记录。

安装包

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from datetime import datetime

from matplotlib.pylab import rcParams

rcParams['figure.figsize']=15,6

一、实验数据

数据集包含了两组数据:Cv值-湿度(float型)以及检测的相对时间(object型)。

#1.数据导入和查看,数据集包含了两组数据:CV Time

data=pd.read_csv('test2.csv',nrows=500)#nrows=80,指加载80组数据

#数据导入和查看

print(data.head())

print('\nData Types:')

print(data.dtypes)

#2.数据格式转换,将数据中的时间信息转换成索引。

#格式转换

dateparse=lambda dates: pd.datetime.strptime(dates, '%Y-%m-%d %H:%M:%S')

data=pd.read_csv('test2.csv', parse_dates=['Time'], index_col='Time', date_parser=dateparse, nrows=80)

# parse_dates:指定包含日期时间信息的列。例子里的列名是'Time‘

# index_col:在TS数据中使用pandas的关键是索引必须是日期等时间变量。所以这个参数告诉pandas使用'Time'列作为索引

# date_parser:它指定了一个将输入字符串转换为datetime可变的函数。pandas 默认读取格式为'YYYY-MM-DD HH:MM:SS'的数据。

# 如果这里的时间格式不一样,就要重新定义时间格式,dataparse函数可以用于此目的。

timeseries = data

print(data.head())

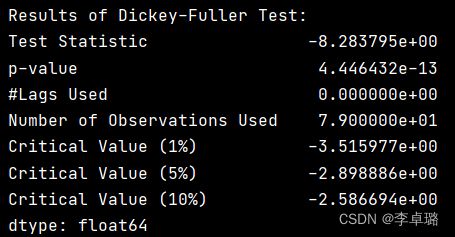

二、检验

1.平稳性检验

判断依据:如果检验统计量(TS)大于临界值(CV),则否决原假设(即序列不是平稳的)。如果TS小于CV,则不能否决原假设(即序列是平稳的)。

#1.平稳性检验

from statsmodels.tsa.stattools import adfuller

#平稳性检测

def test_stationarity(timeseries):

# Determing rolling statistics

rolmean = timeseries.rolling(10).mean()

rolstd = timeseries.rolling(10).std()

# Plot rolling statistics:

plt.plot(timeseries, color='blue', label='Original')

plt.plot(rolmean, color='red', label='Rolling Mean') # 均值

plt.plot(rolstd, color='black', label='Rolling Std') # 标准差

plt.legend(loc='best')

plt.title('Rolling Mean & Standard Deviation')

plt.savefig("./figure/平稳性检测")

plt.show()

# Perform Dickey-Fuller Test:

print('Results of Dickey-Fuller Test:')

dftest = adfuller(timeseries, autolag='AIC')

dfoutput = pd.Series(dftest[0:4], index=['Test Statistic', 'p-value', '#Lags Used', 'Number of Observations Used'])

for key, value in dftest[4].items():

dfoutput['Critical Value (%s)' % key] = value

print(dfoutput)

test_stationarity(timeseries)

实验结果:在所以的置信区间内,TS

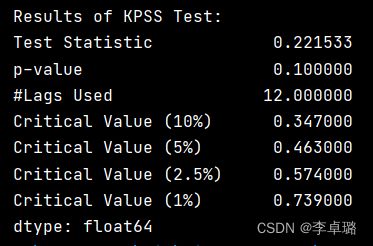

2.KPSS测试

#2.KPSS 测试,不如ADF方法流行。KPSS检验的原假设和备择假设与ADF检验相反。

# define function for ADF

from statsmodels.tsa.stattools import kpss

def kpss_test(timeseries):

print('Results of KPSS Test:')

kpsstest = kpss(timeseries, regression='c')

kpss_output = pd.Series(kpsstest[0:3], index=['Test Statistic', 'p-value', '#Lags Used'])

for key, value in kpsstest[3].items():

kpss_output['Critical Value (%s)' % key] = value

print(kpss_output)

kpss_test(timeseries) #结果显示TS>cv, p <1% 表示拒绝数据是平稳的原假设,序列不是平稳的。

KPSS检验的原假设和备择假设相反。

实验结果:在所以的置信区间内,TS

3.消除趋势

#3.消除趋势,结果显示TS>cv, p <1% 表示拒绝数据是平稳的原假设,序列不是平稳的。

ts_log=np.log(timeseries)

# plt.plot(ts_log)

# plt.show()

#移动平均,根据时间序列的频率取“k”连续值的平均值。

moving_avg = ts_log.rolling(20).mean() #计算均值

ts_log_moving_avg_diff=ts_log-moving_avg #使用均值的差,使得整体平滑

ts_log_moving_avg_diff.dropna(inplace=True) #丢掉NAN

test_stationarity(ts_log_moving_avg_diff)#查看结果

由fig1可以观察到有明显的噪音。因此,利用对数、开方、开立方的方式惩罚最高项,使得整体平滑。

实验结果:TS

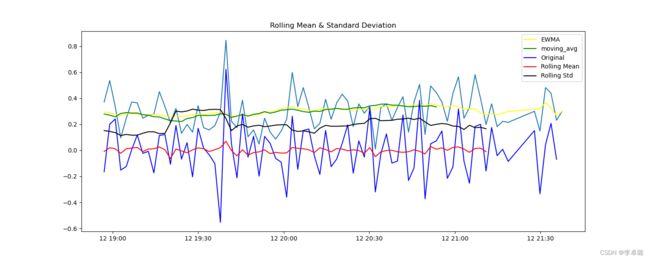

4.EWMA指数加权移动平均

#4.指数加权移动平均(Exponential Weighted Moving Average) 一种流行的方法是指数加权移动平均法,其中权重被分配给所有先前的值,并带有一个衰减因子。

expwighted_avg=pd.DataFrame.ewm(ts_log,halflife=12).mean()

plt.plot(ts_log)

plt.plot(expwighted_avg,color='yellow', label='EWMA')

plt.plot(moving_avg,color='green', label='moving_avg')

ts_log_ewma_diff=ts_log-expwighted_avg

test_stationarity(ts_log_ewma_diff)

实验结果:TS

5.差分

#5.Differencing 差分

ts_log_diff=ts_log-ts_log.shift()

# reduced trend considerably

ts_log_diff.dropna(inplace=True)

test_stationarity(ts_log_diff)

实验结果:TS

三、预测时间序列模型 ARIMA方法

ARIMA(p,d,q)中,AR是“自回归”,p为自回归项数;MA为“滑动平均”,q为滑动平均项数,d为使之成为平稳序列所做的差分次数(阶数)。

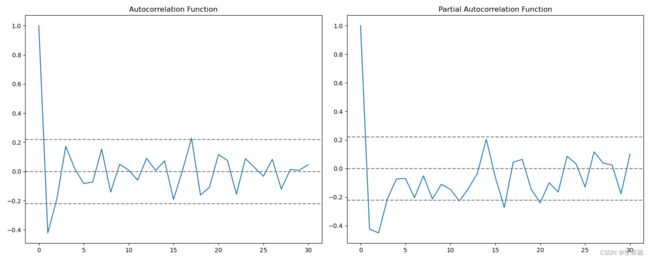

1)ACF;PACF函数

#预测时间序列

from statsmodels.tsa.stattools import acf,pacf

lag_acf=acf(ts_log_diff,nlags=30)

lag_pacf=pacf(ts_log_diff,nlags=30,method='ols')

#1)ACF(Autocorrelation Function),自协方差或自相关函数。

#将有序的随机变量序列与其自身相比较,它反映了同一序列在不同时序的取值之间的相关性。

plt.subplot(121)

plt.plot(lag_acf)

plt.axhline(y=0,linestyle='--',color='gray')

plt.axhline(y=-1.96/np.sqrt(len(ts_log_diff)),linestyle='--',color='gray')

plt.axhline(y=1.96/np.sqrt(len(ts_log_diff)),linestyle='--',color='gray')

plt.title('Autocorrelation Function')

#2)Plot PACF:偏自相关函数(PACF)计算的是严格的两个变量之间的相关性,是剔除了中间变量的干扰之后所得到的两个变量之间的相关程度。

plt.subplot(122)

plt.plot(lag_pacf)

plt.axhline(y=0,linestyle='--',color='gray')

plt.axhline(y=-1.96/np.sqrt(len(ts_log_diff)),linestyle='--',color='gray')

plt.axhline(y=1.96/np.sqrt(len(ts_log_diff)),linestyle='--',color='gray')

plt.title('Partial Autocorrelation Function')

plt.tight_layout()

plt.savefig("./figure/平稳性检测")

plt.show()

Fig5所示。左:ACF(Autocorrelation Function),自协方差或自相关函数。将有序的随机变量序列与其自身相比较,它反映了同一序列在不同时序的取值之间的相关性。直观上来说,ACF 描述了一个观测值和另一个观测值之间的自相关,包括直接和间接的相关性信息。右:PACF:偏自相关函数(PACF)计算的是严格的两个变量之间的相关性,是剔除了中间变量的干扰之后所得到的两个变量之间的相关程度。

其中:p—PACF图第一次穿过置信区间上限的滞后值(0)。q—ACF图第一次穿过置信区间上限的滞后值(0)。

2)AR model 自回归模型

#AR model 自回归模型;是统计上一种处理时间序列的方法,用同一变数例如x的之前各期,亦即x1至xt-1来预测本期xt的表现,并假设它们为一线性关系。

from statsmodels.tsa.arima_model import ARIMA

model = ARIMA(ts_log,order=(2,1,0))

results_AR=model.fit(disp=-1)

result=pd.DataFrame(results_AR.fittedvalues, columns=['CV'])

plt.plot(ts_log_diff,color='blue', label='ts_log')

plt.plot(results_AR.fittedvalues,color='red', label='results_AR')

plt.title('RSS: %.4f'% ((result-ts_log_diff)**2).sum())#RSS是残差值

plt.savefig("./figure/平稳性检测")

plt.show()

AR是统计上一种处理时间序列的方法,用同一变数例如x的之前各期,亦即x1至xt-1来预测本期xt的表现,并假设它们为一线性关系。其中,RSS是残差值=1.95。

3)MA model 移动平均模型

#MA model 移动平均模型关注的是自回归模型中的误差项的累加。它能够有效地消除预测中的随机波动。

model = ARIMA(ts_log,order=(0,1,2))

results_MA=model.fit(disp=-1)

result=pd.DataFrame(results_MA.fittedvalues, columns=['CV'])

plt.plot(ts_log_diff,color='blue', label='ts_log')

plt.plot(results_MA.fittedvalues,color='red', label='results_MA')

plt.title('RSS: %.4f'% ((result-ts_log_diff)**2).sum())

plt.savefig("./figure/平稳性检测")

plt.show()

MA关注的是自回归模型中的误差项的累加。它能够有效地消除预测中的随机波动。RSS=1.6569。

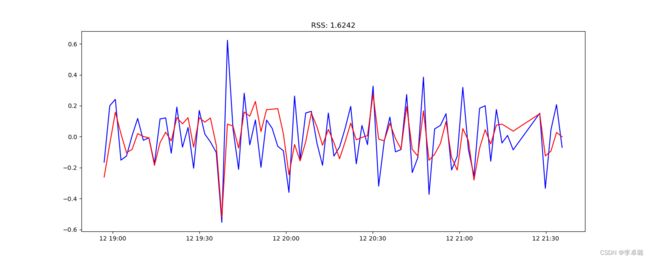

4)组合模型

#组合模型

model = ARIMA(ts_log,order=(2,1,2))

results_ARIMA=model.fit(disp=-1)

result=pd.DataFrame(results_ARIMA.fittedvalues, columns=['CV'])

plt.plot(ts_log_diff,color='blue', label='ts_log')

plt.plot(results_ARIMA.fittedvalues,color='red', label='results_ARIMA')

plt.title('RSS: %.4f'% ((result-ts_log_diff)**2).sum())

plt.savefig("./figure/平稳性检测")

plt.show()

RSS=1.6242。 Fig8发现MA和组合差不多,结果要比AR效果好。