【时间序列 - 02】ExponentialSmoothing - 指数平滑算法

Abstract:

本文主要以实践的角度介绍指数平滑算法,包括:1)使用 ExponentialSmoothing 框架调用指数平滑算法;2)文末附有“使用python实现指数平滑算法(不确定写得对不对,T_T)”。此外,指数平滑算法的理论知识以参考链接的方式进行整理。

Reference

https://www.statsmodels.org/stable/generated/statsmodels.tsa.holtwinters.ExponentialSmoothing.html?highlight=exponentialsmoothing

指数平滑算法理论知识:

- MBA-Lib:wiki,指数平滑算法

- https://blog.csdn.net/nieson2012/article/details/51980943

Knowledge

class statsmodels.tsa.holtwinters.ExponentialSmoothing(endog, trend=None, damped=False, seasonal=None, seasonal_periods=None, dates=None, freq=None, missing='none')

Holt Winter's Exponential Smoothing

| Parameters: |

|

| Returns: |

results |

| Return type: |

ExponentialSmoothing class |

调用模型

model = ExponentialSmoothing(train, seasonal='additive', seasonal_periods = seasonal_periods).fit()

pred = model.predict(start=test.index[0], end=test.index[-1])

## fit(self, smoothing_level=None, smoothing_slope=None, smoothing_seasonal=None,

damping_slope=None, optimized=True, use_boxcox=False, remove_bias=False,

use_basinhopping=False)

## 若需详细了解 - 建议看源码

## https://www.statsmodels.org/stable/_modules/statsmodels/tsa/holtwinters.html#ExponentialSmoothing

smoothing_level=None ## alpha

smoothing_slope=None ## beta

smoothing_seasonal=None ## gamma

damping_slope=None ## phi value of the damped method

optimized=True ## hould the values that have not been set above be optimized automatically?

use_boxcox=False ## {True, False, 'log', float} log->apply log; float->lambda equal to float.

remove_bias=False ##

use_basinhopping=False ## Should the opptimser try harder using basinhopping to find optimal values?调参

class ExponentialSmoothing/fit()

1. use_boxcox

-

use_boxcox = False(predict 201710~11)

-

use_boxcox = 'log'(predict 201710~11)

2. use_basinhopping

-

use_basinhopping = False

-

use_basinhopping = True

-

参数组合:use_basinhopping = True, use_boxcox = 'log'(predict 201710~11)

上述参数对应模型的泛化能力有待提升,当预测 201610~11时,效果相反,即 use_boxcox=False, use_basinhopping = False 这组参数的效果更好。

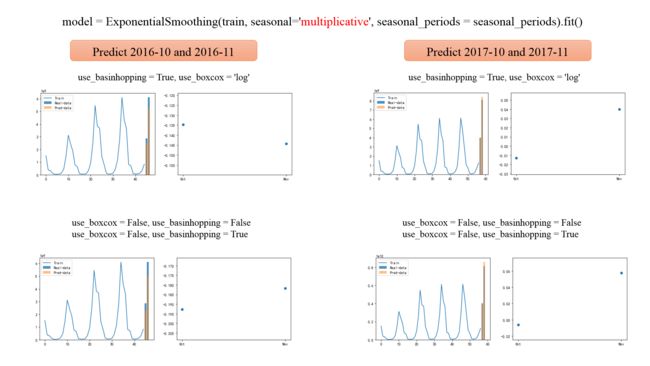

class ExponentialSmoothing(seasonal)

-

seasonal = "add" - "additive" ## 累乘式

-

seasonal = "mul" - "multiplicative" ## 累加式

-

seasonal = "None"

-

seasonal = "mul",use_basinhopping = True, use_boxcox = 'log' ## 效果相对更优

Source code for statsmodels.tsa.holtwinters

-

引用文件

import numpy as np

from statsmodels.base.model import Results

from statsmodels.base.wrapper import populate_wrapper, union_dicts, ResultsWrapper

from statsmodels.tsa.base.tsa_model import TimeSeriesModel

from scipy.optimize import basinhopping, brute, minimize

from scipy.spatial.distance import sqeuclidean

try:

from scipy.special import inv_boxcox

except ImportError:

def inv_boxcox(x, lmbda):

return np.exp(np.log1p(lmbda * x) / lmbda) if lmbda != 0 else np.exp(x)

from scipy.stats import boxcox-

class HoltWintersResults(Results)

-

class HoltWintersResultsWrapper(ResultsWrapper)

-

class ExponentialSmoothing(TimeSeriesModel)

-

class SimpleExpSmoothing(ExponentialSmoothing)

-

class Holt(ExponentialSmoothing)

My Script - 20180716

import pandas as pd

#import numpy as np

import matplotlib.pyplot as plt

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from hcq_lib import cal_error, hcq_write

month_list = ["Jan","Feb","Mar","Apr","May","June",

"July","Aug","Sept","Oct","Nov","Dec"]

all_leaf_class_name_dict = {cate_id: cate_name}

# =============================================================================

# Meta-Parameters

# =============================================================================

seasonal = 'multiplicative'

#seasonal = 'add'

use_basinhopping = True

use_boxcox='log'

#use_boxcox=False

seasonal_periods = 12

len_pred = 2 ## 预测月数

#stop_month_list = ["2015-02", "2015-03", "2015-04", "2015-05", "2015-06", "2015-07",

# "2015-08", "2015-09", "2015-10", "2015-11", "2015-12"]

#

stop_month_list = ["2016-02", "2016-03", "2016-04", "2016-05", "2016-06", "2016-07",

"2016-08", "2016-09", "2016-10", "2016-11", "2016-12"]

#stop_month_list = ["2017-02", "2017-03", "2017-04", "2017-05", "2017-06", "2017-07",

# "2017-08", "2017-09", "2017-10", "2017-11", "2017-12"]

#stop_month = "2015-12" ## format "xxxx-xx"w

log_path = "./log/statsmodels_ExponentialSmoothing.txt"

df = pd.read_csv('./dataset/cate_by_month_histroy.csv', header=0, encoding='gbk')

df.columns = ['ds', 'cate_id', 'cate_name', 'y']

for cate_id in all_leaf_class_name_dict.keys():

cate_name = all_leaf_class_name_dict[cate_id]

## 传入的.csv数据是全部的历史数据

## 此处提供设置选取部分数据作为实验数据

## 如,截取包括"2017-12"之前的数据作为实验数据,然后再进行train和val数据集的切分

error_info = ""

for stop_month in stop_month_list:

class_df_all = df[df.cate_name.str.startswith(cate_name)].reset_index(drop=True)

stop_month_index = class_df_all[class_df_all.ds == stop_month].index.tolist()[0]

print(stop_month, stop_month_index)

class_df_all = class_df_all[:stop_month_index+1]

len_dataset = len(class_df_all)

train, test = class_df_all['y'][:len_dataset-len_pred], class_df_all['y'][len_dataset-len_pred:]

## seasonal: {"add", "mul", "additive", "multiplicative", None}

# model = ExponentialSmoothing(train, seasonal='additive', seasonal_periods = seasonal_periods).fit(smoothing_level=0.25)

# model = ExponentialSmoothing(train, seasonal='multiplicative', seasonal_periods = seasonal_periods).fit(use_boxcox=False, use_basinhopping = False)

# model = ExponentialSmoothing(train, seasonal='additive', seasonal_periods = seasonal_periods).fit(use_boxcox='log')

model = ExponentialSmoothing(train, seasonal=seasonal, seasonal_periods = seasonal_periods).fit(

use_basinhopping = use_basinhopping, use_boxcox=use_boxcox)

pred = model.predict(start=test.index[0], end=test.index[-1]) ## 56, 59

## error

error_list = cal_error(pred, test)

for _error in error_list:

error_info += (str(_error) + " ")

hcq_write(log_path, True, True, "==== {} ====".format(cate_name))

parameters_info = "seasonal = {}, use_basinhopping = {}, use_boxcox = {}, seasonal_periods = {} ||| len_pred = {}".format(

seasonal, use_basinhopping, use_boxcox, seasonal_periods, len_pred)

hcq_write(log_path, True, True, parameters_info)

hcq_write(log_path, False, True, error_info)

# =============================================================================

# # plot

# fig = plt.figure(facecolor='white')

# ax = fig.add_subplot(121)

# ax.plot(train.index, train, label='Train')

# ax.bar(test.index, test, alpha=0.8, label='Real-data')

# ax.bar(pred.index, pred, alpha=0.5, label='Pred-data')

# ax.set_xlabel('Time Series of days')

# ax.set_ylabel('GMV: Gross Merchandise Volume')

# ax.set_title(u'{}: {} ||| predict {} month'.format(cate_name, stop_month, len_pred))

# plt.legend(loc='best')

#

# ax_error = fig.add_subplot(122)

# ax_error.scatter(month_list[int(stop_month.split("-")[1])-len_pred:int(stop_month.split("-")[1])], error_list, label='error')

#

# fig.set_size_inches(12, 4)

# plt.savefig("./plot_history_data/{}-{}".format(cate_name, stop_month))python:实现指数平滑算法

# -*- coding: utf-8 -*-

# @Date : 2017-04-11 21:27:00

# @Author : Alan Lau ([email protected])

# @Language : Python3.5

# https://blog.csdn.net/AlanConstantineLau/article/details/70173561

import numpy as np

from matplotlib import pyplot as plt

plt.rcParams['font.sans-serif']=['SimHei']

plt.rcParams['axes.unicode_minus']=False

import xlrd

all_leaf_class_name_list = ['毛针织衫', '休闲运动套装']

file_path = './dataset/target_leaf_level_0625_by_month.csv'

file = xlrd.open_workbook(file_path)

class_name_list = all_leaf_class_name_list

#alpha = 0.47 #设置alphe,即平滑系数

#指数平滑公式

def exponential_smoothing(alpha, s):

s_out = np.zeros(len(s))

# s_result[0] = float(s[1]+s[2]+s[3])/3

s_out[0] = s[0]

for i in range(1, len(s_out)):

s_out[i] = alpha*s[i]+(1-alpha)*s_out[i-1]

return s_out

# =============================================================================

# 循环尝试 alpha 平滑系数:横轴表示alpha,纵轴表示模型误差

# 误差计算方法:sum(所有预测值 - 所有真实值) / sum(所有真实值)

# =============================================================================

alpha_list = [x for x in np.arange(0.1, 1.0, 0.005)]

def show_data_alpha(GMV_list_true, class_name, RMSE_double_list, RMSE_triple_list, bset_alpha_double, RMSE_bset_alpha_double, bset_alpha_triple, RMSE_bset_alpha_triple):

plt.figure(figsize=(10, 6), dpi=80)#设置绘图区域的大小和像素

plt.plot(alpha_list, RMSE_double_list, color='red', label="double predicted, bset_alpha_double = {}, s_RMSE = {}".format(

bset_alpha_double, RMSE_bset_alpha_double)) # 将二次指数平滑法计算的预测值的折线设置为红色

plt.plot(alpha_list, RMSE_triple_list, color='green', label="triple predicted, bset_alpha_triple = {}, s_RMSE = {}".format(

bset_alpha_triple, RMSE_bset_alpha_triple)) # 将三次指数平滑法计算的预测值的折线设置为绿色

plt.legend(loc='upper left') # 显示图例的位置,这里为左上方

plt.title('{}_alpha_finding'.format(class_name))

plt.ylabel('MAPE') # y轴标签

plt.savefig("./result_exponential_smoothing_2/{}".format(class_name + "_find_best_alpha"))

def load_data(table_sheet, data_stop_index):

year_month_list = []

GMV_list = []

GMV_list_true = []

# nrows = table_sheet.nrows

## row=40 --> 201803

row = data_stop_index

for i in range(row-1):

year_month_list.append(table_sheet.col(0)[i+1].value)

GMV_list.append(float(table_sheet.col(1)[i+1].value))

GMV_list_true.append(float(table_sheet.col(1)[i+1].value))

GMV_list_true.append(float(table_sheet.col(1)[row].value))

# print("GMV_list_true = {}".format(GMV_list_true))

# print(float(table_sheet.col(6)[40].value))

# print(float(table_sheet.col(6)[41].value))

# print(len(GMV_list))

return year_month_list, GMV_list, GMV_list_true

# =============================================================================

# author: 初类

# date: 20180619

# 功能:基于历史数据,分别计算二次平滑指数模型和三次平滑指数模型的预测值

# 1)validation 集合:2018年2月~4月;test 集合:2018年5月

# 2)预测2018年2月份:使用2015年1月~2018年1月的历史实际数据;预测2018年3月时,引入2018年2月份的真是数据。

# =============================================================================

## data_stop_index:训练数据的截止点。如,预测2018年2月份时,data_stop指向2018年1月份

## data_stop_index = 38 --> 201801(取得到)

## data_stop_index = 39 --> 201802(取得到)

validation_month_index = [60] ## 201802, 201803, 201804

def main():

for class_name in class_name_list:

## 依次尝试每个平滑系数

RMSE_double_list = []

RMSE_triple_list = []

avg_RMSE_bset_alpha_double = 999

avg_RMSE_bset_alpha_triple = 999

bset_alpha_double = alpha_list[0]

bset_alpha_triple = alpha_list[0]

for alpha in alpha_list:

# print("alpha = {}".format(alpha))

RMSE_double = 0

RMSE_triple = 0

try:

table_sheet = file.sheet_by_name(class_name)

for data_stop_index in validation_month_index:

year_month_list, GMV_list, GMV_list_true = load_data(table_sheet, data_stop_index)

# =============================================================================

# reference: http://wiki.mbalib.com/wiki/%E6%8C%87%E6%95%B0%E5%B9%B3%E6%BB%91%E6%B3%95

# =============================================================================

s_single = exponential_smoothing(alpha, GMV_list)

s_double = exponential_smoothing(alpha, s_single)

a_double = 2*s_single-s_double # 计算二次指数平滑的a

b_double = (alpha/(1-alpha))*(s_single-s_double) # 计算二次指数平滑的b

s_pre_double = np.zeros(s_double.shape) # 建立预测轴

for i in range(0, len(GMV_list)):

# 循环计算每一年的二次指数平滑法的预测值,下面三次指数平滑法原理相同

s_pre_double[i] = a_double[i] + b_double[i]

pre_next_year = a_double[-1]+b_double[-1]*1 # 预测下一个月

s_pre_double = np.insert(s_pre_double, len(s_pre_double), values=np.array([pre_next_year]), axis=0)

### 三次平滑指数

s_triple = exponential_smoothing(alpha, s_double)

a_triple = 3*s_single-3*s_double+s_triple

b_triple = (alpha/(2*((1-alpha)**2)))*((6-5*alpha)*s_single -2*((5-4*alpha)*s_double)+(4-3*alpha)*s_triple)

c_triple = ((alpha**2)/(2*((1-alpha)**2)))*(s_single-2*s_double+s_triple)

s_pre_triple = np.zeros(s_triple.shape)

for i in range(0, len(GMV_list)):

s_pre_triple[i] = a_triple[i]+b_triple[i]*1 + c_triple[i]*(1**2)

pre_next_year = a_triple[-1]+b_triple[-1]*1 + c_triple[-1]*(1**2)

s_pre_triple = np.insert(s_pre_triple, len(s_pre_triple), values=np.array([pre_next_year]), axis=0)

=============================================================================

# 计算误差

# =============================================================================

final_month_num = -1

sum_ture_test = np.sum(GMV_list_true[final_month_num])

# print("[alpha = {}] sum_ture_test = {}, s_pre_double = {}, s_pre_triple = {}".format(

# round(alpha, 2), sum_ture_test, s_pre_double[final_month_num], s_pre_triple[final_month_num]))

RMSE_double += ((np.sum((s_pre_double[final_month_num] - GMV_list_true[final_month_num])**2))**0.5)/sum_ture_test

RMSE_triple += ((np.sum((s_pre_triple[final_month_num] - GMV_list_true[final_month_num])**2))**0.5)/sum_ture_test

RMSE_double = round(RMSE_double/len(validation_month_index), 8)

RMSE_triple = round(RMSE_triple/len(validation_month_index), 8)

# print("RMSE_double = {}, RMSE_triple = {}".format(RMSE_double, RMSE_triple))

if RMSE_double < avg_RMSE_bset_alpha_double:

avg_RMSE_bset_alpha_double = RMSE_double

bset_alpha_double = round(alpha, 2)

if RMSE_triple < avg_RMSE_bset_alpha_triple:

avg_RMSE_bset_alpha_triple = RMSE_triple

bset_alpha_triple = round(alpha, 2)

RMSE_double_list.append(RMSE_double)

RMSE_triple_list.append(RMSE_triple)

except Exception as e:

print("except [{}] {}".format(class_name, e))

## show plot

show_data_alpha(GMV_list_true, class_name, RMSE_double_list, RMSE_triple_list,

bset_alpha_double, avg_RMSE_bset_alpha_double, bset_alpha_triple, avg_RMSE_bset_alpha_triple)

if __name__ == '__main__':

main()