kaggle-房价预测案例

此案例为kaggle上面的房价预测案例

https://www.kaggle.com/c/house-prices-advanced-regression-techniques

具体代码如下

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

#-------------------Step1:读取数据---------------------

train_df=pd.read_csv('C:\\Users\\Administrator\\Desktop\\network\\House_prise\\train.csv')

test_df=pd.read_csv('C:\\Users\\Administrator\\Desktop\\network\\House_prise\\test.csv')

#查看数据前5行

print(train_df.head())

print(test_df.head())

'''

Id MSSubClass MSZoning ... SaleType SaleCondition SalePrice

0 1 60 RL ... WD Normal 208500

1 2 20 RL ... WD Normal 181500

2 3 60 RL ... WD Normal 223500

3 4 70 RL ... WD Abnorml 140000

4 5 60 RL ... WD Normal 250000

[5 rows x 81 columns]

Id MSSubClass MSZoning ... YrSold SaleType SaleCondition

0 1461 20 RH ... 2010 WD Normal

1 1462 20 RL ... 2010 WD Normal

2 1463 60 RL ... 2010 WD Normal

3 1464 60 RL ... 2010 WD Normal

4 1465 120 RL ... 2010 WD Normal

[5 rows x 79 columns]

'''

#-----------------------------------Step2:合并数据---------------------------------

#这么做是为了把训练集和测试集的数据一块来一次性处理,等到处理完后再将他们分开

#上面在训练集中的最后一个属性SalePrice为我们的训练目标,因此只出现在训练集中,所以我们先将它

#作为y_train拿出来

#我们先看SalePrice长什么样

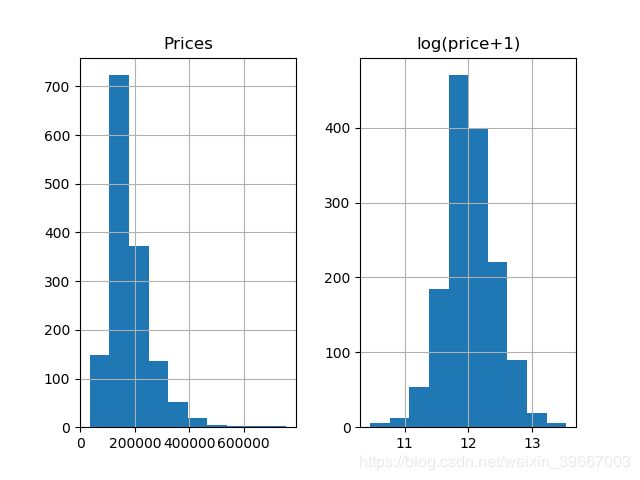

prices=pd.DataFrame({'Prices':train_df['SalePrice'],'log(price+1)':np.log1p(train_df['SalePrice'])})

print(prices.hist())

plt.show()

从上图可以看出,测试集中的预测目标‘SalePrice’特征并不正态化,为了让我们的预测目标平滑一些,我们可以使用log(X+1)即log1p,所得结果如右图所示。需要注意的是,最后计算结果的时候,记得把预测到的平滑数据变回去,使用expm1().

#将train_df中的属性‘SalePrice’取出给y_train,此时train_df中就没有这一属性了

y_train=np.log1p(train_df.pop('SalePrice'))

#将剩余部分按照行合并起来

all_df=pd.concat((train_df,test_df),axis=0)

#查看合并后的形状

print(all_df.shape)

'''

(2919, 79)

'''

print(y_train.head())#查看y_train

'''

0 12.247699

1 12.109016

2 12.317171

3 11.849405

4 12.429220

Name: SalePrice, dtype: float64

'''

#-----------------------------------Step3: 变量转换-----------------------------------

#首先我们观察到'MSSubClass'的值虽然用不同的数字表示,但它应该是一些类别,我们要将它变回string类型

print(all_df['MSSubClass'].dtypes)

'''

int64

'''

all_df['MSSubClass']=all_df['MSSubClass'].astype(str)

#变成str后,做个统计就清楚了

print(all_df['MSSubClass'].value_counts())

'''

20 1079

60 575

50 287

120 182

30 139

160 128

70 128

80 118

90 109

190 61

85 48

75 23

45 18

180 17

40 6

150 1

Name: MSSubClass, dtype: int64

'''

#把category的变量转变成numerical表达形式

print(pd.get_dummies(all_df['MSSubClass'],prefix='MSSubClass').head())#此刻MSSubClass被我们分成了16个column,每一个代表一个category。是就是1,不是就是0。

'''

MSSubClass_120 MSSubClass_150 ... MSSubClass_85 MSSubClass_90

0 0 0 ... 0 0

1 0 0 ... 0 0

2 0 0 ... 0 0

3 0 0 ... 0 0

4 0 0 ... 0 0

[5 rows x 16 columns]

'''

#同理,我们把所有的catagory数据都使用one-hot编码

all_dummy_df=pd.get_dummies(all_df)

print(all_dummy_df.head())

'''

Id ... SaleCondition_Partial

0 1 ... 0

1 2 ... 0

2 3 ... 0

3 4 ... 0

4 5 ... 0

[5 rows x 303 columns]

'''

#对缺失值的处理

#查看缺失值,计算每个属性的缺失值个数,将其按照从多到少排序

print(all_dummy_df.isnull().sum().sort_values(ascending=False).head(10))

'''

[5 rows x 303 columns]

LotFrontage 486

GarageYrBlt 159

MasVnrArea 23

BsmtFullBath 2

BsmtHalfBath 2

GarageCars 1

BsmtFinSF1 1

BsmtFinSF2 1

BsmtUnfSF 1

TotalBsmtSF 1

dtype: int64

'''

#可以看到,缺失最多的column是LotFrontage

#在这里,我们用平均值来填满这些空缺。

mean_cols=all_dummy_df.mean()

all_dummy_df=all_dummy_df.fillna(mean_cols)

#查看是否还有空缺值

print(all_dummy_df.isnull().sum().sum())

'''

0

'''

#标准化数据

#我们不需要把One-Hot的那些0/1数据给标准化。我们的目标是那些本来就是numerical的数据

numeric_cols=all_df.columns[all_df.dtypes!='object']

print(numeric_cols)

#计算标准分布(X-X')/S

numeric_cols_means=all_dummy_df.loc[:,numeric_cols].mean()

numeric_cols_std=all_dummy_df.loc[:,numeric_cols].std()

all_dummy_df.loc[:,numeric_cols]=(all_dummy_df.loc[:,numeric_cols]-numeric_cols_means)/numeric_cols_std

#-------------------------------Step 4:建立模型-----------------------------------------

#把数据集分回训练/测试集

dummy_train_df=all_dummy_df.loc[train_df.index]

dummy_test_df=all_dummy_df.loc[test_df.index]

print(dummy_train_df.shape,dummy_test_df.shape)

'''

(1460, 303) (1459, 303)

'''

#岭回归

#对于多因子的数据集,这种模型可以方便的把所有的var都无脑的放进去

from sklearn.linear_model import Ridge

from sklearn.model_selection import cross_val_score

#这一步不是很必要,只是把DF转化成Numpy Array,这跟Sklearn更加配

X_train=dummy_train_df.values

X_test=dummy_test_df.values

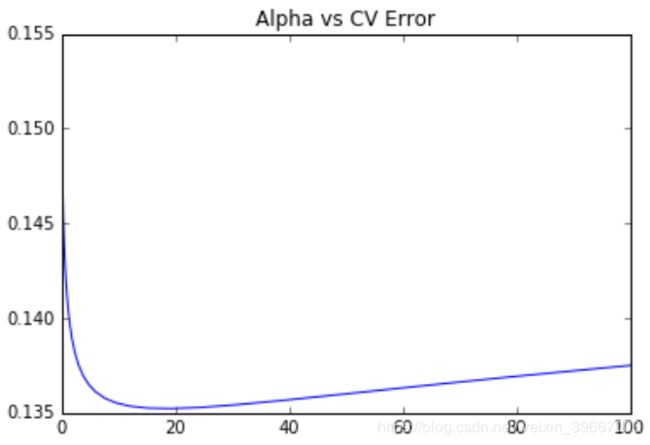

#用Sklearn自带的cross validation方法来测试模型

alphas=np.logspace(-3,2,50)

test_scores=[]

for alpha in alphas:

clf=Ridge(alpha)

test_score=np.sqrt(-cross_val_score(clf,X_train,y_train,cv=10,scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

#存下所有的CV值,看看哪个alpha值更好

plt.plot(alphas,test_scores)

plt.title("Alpha vs CV Error")

plt.show()

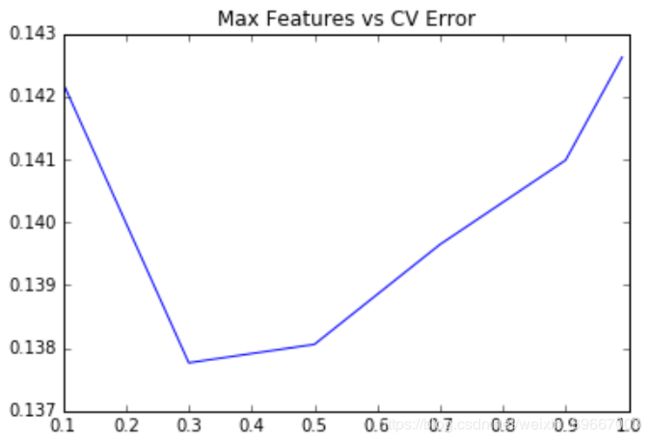

#随机森林

from sklearn.ensemble import RandomForestRegressor

max_features=[.1,.3,.5,.7,.9,.99]

test_scores=[]

for max_feature in max_features:

clf=RandomForestRegressor(n_estimators=200,max_features=max_feature)

test_score=np.sqrt(-cross_val_score(clf,X_train,y_train,cv=5,scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

plt.plot(max_features,test_scores)

plt.title('Max Features vs CV Error')

plt.show()

#--------------------------------Step5:模型融合----------------------------------

#这里我们用一个Stacking的思维来汲取两种或者多种模型的优点

#首先,我们把最好的parameter拿出来,做成我们最终的model

ridge=Ridge(alpha=15)

rf=RandomForestRegressor(n_estimators=500,max_features=.3)

ridge.fit(X_train,y_train)

rf.fit(X_train,y_train)

#上面提到了,因为最前面我们给label做了个log(1+x), 于是这里我们需要把predit的值给exp回去,并且减掉那个"1"

#所以就是我们的expm1()函数。

y_ridge=np.expm1(ridge.predict(X_test))

y_rf=np.expm1(rf.predict(X_test))

#一个正经的Ensemble是把这群model的预测结果作为新的input,再做一次预测。这里我们简单的方法,就是直接『平均化』。

y_final=(y_ridge+y_rf)/2

#-----------------------------------------Step6:提交结果--------------------------------------

submission_df=pd.DataFrame(data={'Id':test_df.index,'SalePrice':y_final})

print(submission_df.head(10))

'''

Id SalePrice

0 1461 118872.530547

1 1462 150845.024158

2 1463 175443.392106

3 1464 190153.672131

4 1465 195473.772773

5 1466 176301.877235

6 1467 177621.182529

7 1468 169012.173189

8 1469 184472.271054

9 1470 122613.992701

'''由于单个分类器效果是有限的,我们可以把N多个分类器合在一起,做一个综合分类器达到最好的效果。

#Bagging

#Bagging把很多的小分类器放在一起,每个train随机的一部分数据,然后把它们的最终结果综合起来(多数投票制)。

from sklearn.ensemble import BaggingRegressor

params = [1, 10, 15, 20, 25, 30, 40]

test_scores = []

for param in params:

clf = BaggingRegressor(n_estimators=param, base_estimator=ridge)#使用上面的小分类器ridge

test_score = np.sqrt(-cross_val_score(clf, X_train, y_train, cv=10, scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

plt.plot(params, test_scores)

plt.title("n_estimator vs CV Error")

#使用Bagging自带的DecisionTree模型

params = [10, 15, 20, 25, 30, 40, 50, 60, 70, 100]

test_scores = []

for param in params:

clf = BaggingRegressor(n_estimators=param)

test_score = np.sqrt(-cross_val_score(clf, X_train, y_train, cv=10, scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

plt.plot(params, test_scores)

plt.title("n_estimator vs CV Error")

#Boosting

#Boosting比Bagging理论上更高级点,它也是揽来一把的分类器。但是把他们线性排列。

#下一个分类器把上一个分类器分类得不好的地方加上更高的权重,这样下一个分类器就能在这个部分学得更加“深刻”。

from sklearn.ensemble import AdaBoostRegressor

params = [10, 15, 20, 25, 30, 35, 40, 45, 50]

test_scores = []

for param in params:

clf = BaggingRegressor(n_estimators=param, base_estimator=ridge)

test_score = np.sqrt(-cross_val_score(clf, X_train, y_train, cv=10, scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

plt.plot(params, test_scores)

plt.title("n_estimator vs CV Error")

#最后,我们来看看巨牛逼的XGBoost,外号:Kaggle神器

#这依旧是一款Boosting框架的模型,但是却做了很多的改进。

from xgboost import XGBRegressor

params=[1,2,3,4,5,6]

test_scores=[]

for param in params:

clf=XGBRegressor(max_depth=param)

test_score=np.sqrt(-cross_val_score(clf,X_train,y_train,cv=10,scoring='neg_mean_squared_error'))

test_scores.append(np.mean(test_score))

plt.plot(params,test_scores)

plt.title('max_depth vs CV Error')