线性回归

线性回归模型与诊断

数据说明:本数据是一份汽车贷款数据

| 字段名 | 中文含义 |

|---|---|

| id | id |

| Acc | 是否开卡(1=已开通) |

| avg_exp | 月均信用卡支出(元) |

| avg_exp_ln | 月均信用卡支出的自然对数 |

| gender | 性别(男=1) |

| Age | 年龄 |

| Income | 年收入(万元) |

| Ownrent | 是否自有住房(有=1;无=0) |

| Selfempl | 是否自谋职业(1=yes, 0=no) |

| dist_home_val | 所住小区房屋均价(万元) |

| dist_avg_income | 当地人均收入 |

| high_avg | 高出当地平均收入 |

| edu_class | 教育等级:小学及以下开通=0,中学=1,本科=2,研究生=3 |

%matplotlib inline

import matplotlib.pyplot as plt

import os

import numpy as np

import pandas as pd

import statsmodels.api as sm

from statsmodels.formula.api import ols

os.chdir('E:/data')

pd.set_option('display.max_columns', 8)

E:\Anaconda3\lib\site-packages\statsmodels\compat\pandas.py:56: FutureWarning: The pandas.core.datetools module is deprecated and will be removed in a future version. Please use the pandas.tseries module instead.

from pandas.core import datetools

导入数据和数据清洗

raw = pd.read_csv('creditcard_exp.csv', skipinitialspace=True)

raw.head()

| id | Acc | avg_exp | avg_exp_ln | ... | dist_avg_income | age2 | high_avg | edu_class | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 19 | 1 | 1217.03 | 7.104169 | ... | 15.932789 | 1600 | 0.102361 | 3 |

| 1 | 5 | 1 | 1251.50 | 7.132098 | ... | 15.796316 | 1024 | 0.051184 | 2 |

| 2 | 95 | 0 | NaN | NaN | ... | 7.490000 | 1296 | 0.910000 | 1 |

| 3 | 86 | 1 | 856.57 | 6.752936 | ... | 11.275632 | 1681 | 0.197218 | 3 |

| 4 | 50 | 1 | 1321.83 | 7.186772 | ... | 13.346474 | 784 | 0.062676 | 2 |

5 rows × 14 columns

exp = raw[raw['avg_exp'].notnull()].copy().iloc[:, 2:]\

.drop('age2',axis=1)

exp_new = raw[raw['avg_exp'].isnull()].copy().iloc[:, 2:]\

.drop('age2',axis=1)

exp.describe(include='all')

| avg_exp | avg_exp_ln | gender | Age | ... | dist_home_val | dist_avg_income | high_avg | edu_class | |

|---|---|---|---|---|---|---|---|---|---|

| count | 70.000000 | 70.000000 | 70.000000 | 70.000000 | ... | 70.000000 | 70.000000 | 70.000000 | 70.000000 |

| mean | 983.655429 | 6.787787 | 0.285714 | 31.157143 | ... | 74.540857 | 8.005472 | -0.580766 | 1.928571 |

| std | 446.294237 | 0.476035 | 0.455016 | 7.206349 | ... | 36.949228 | 3.070744 | 0.432808 | 0.873464 |

| min | 163.180000 | 5.094854 | 0.000000 | 20.000000 | ... | 13.130000 | 3.828842 | -1.526850 | 0.000000 |

| 25% | 697.155000 | 6.547003 | 0.000000 | 26.000000 | ... | 49.302500 | 5.915553 | -0.887981 | 1.000000 |

| 50% | 884.150000 | 6.784627 | 0.000000 | 30.000000 | ... | 65.660000 | 7.084184 | -0.612068 | 2.000000 |

| 75% | 1229.585000 | 7.114415 | 1.000000 | 36.000000 | ... | 105.067500 | 9.123105 | -0.302082 | 3.000000 |

| max | 2430.030000 | 7.795659 | 1.000000 | 55.000000 | ... | 157.900000 | 18.427000 | 0.259337 | 3.000000 |

8 rows × 11 columns

相关性分析

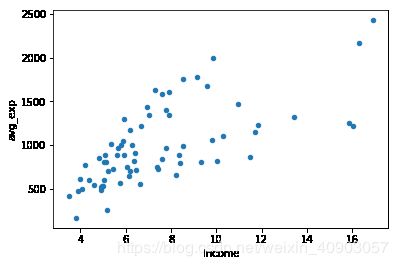

散点图

exp.plot('Income', 'avg_exp', kind='scatter')

plt.show()

[外链图片转存 (img-0SGvSTVL-1562725477539)(output_7_0.png)]

(img-0SGvSTVL-1562725477539)(output_7_0.png)]

exp[['Income', 'avg_exp', 'Age', 'dist_home_val']].corr(method='pearson')

| Income | avg_exp | Age | dist_home_val | |

|---|---|---|---|---|

| Income | 1.000000 | 0.674011 | 0.369129 | 0.249153 |

| avg_exp | 0.674011 | 1.000000 | 0.258478 | 0.319499 |

| Age | 0.369129 | 0.258478 | 1.000000 | 0.109323 |

| dist_home_val | 0.249153 | 0.319499 | 0.109323 | 1.000000 |

线性回归算法

简单线性回归

lm_s = ols('avg_exp ~ Income', data=exp).fit()

print(lm_s.params)

Intercept 258.049498

Income 97.728578

dtype: float64

Predict-在原始数据集上得到预测值和残差

lm_s.summary()

| Dep. Variable: | avg_exp | R-squared: | 0.454 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.446 |

| Method: | Least Squares | F-statistic: | 56.61 |

| Date: | Mon, 30 Apr 2018 | Prob (F-statistic): | 1.60e-10 |

| Time: | 16:59:33 | Log-Likelihood: | -504.69 |

| No. Observations: | 70 | AIC: | 1013. |

| Df Residuals: | 68 | BIC: | 1018. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 258.0495 | 104.290 | 2.474 | 0.016 | 49.942 | 466.157 |

| Income | 97.7286 | 12.989 | 7.524 | 0.000 | 71.809 | 123.648 |

| Omnibus: | 3.714 | Durbin-Watson: | 1.424 |

|---|---|---|---|

| Prob(Omnibus): | 0.156 | Jarque-Bera (JB): | 3.507 |

| Skew: | 0.485 | Prob(JB): | 0.173 |

| Kurtosis: | 2.490 | Cond. No. | 21.4 |

pd.DataFrame([lm_s.predict(exp), lm_s.resid], index=['predict', 'resid']

).T.head()

| predict | resid | |

|---|---|---|

| 0 | 1825.141904 | -608.111904 |

| 1 | 1806.803136 | -555.303136 |

| 3 | 1379.274813 | -522.704813 |

| 4 | 1568.506658 | -246.676658 |

| 5 | 1238.281793 | -422.251793 |

在待预测数据集上得到预测值

lm_s.predict(exp_new)[:5]

2 1078.969552

11 756.465245

13 736.919530

19 687.077955

20 666.554953

dtype: float64

多元线性回归

lm_m = ols('avg_exp ~Income + dist_home_val + dist_avg_income',

data=exp).fit()

lm_m.summary()

| Dep. Variable: | avg_exp | R-squared: | 0.541 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.520 |

| Method: | Least Squares | F-statistic: | 25.95 |

| Date: | Mon, 30 Apr 2018 | Prob (F-statistic): | 3.34e-11 |

| Time: | 16:59:33 | Log-Likelihood: | -498.62 |

| No. Observations: | 70 | AIC: | 1005. |

| Df Residuals: | 66 | BIC: | 1014. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 2.3507 | 122.525 | 0.019 | 0.985 | -242.278 | 246.980 |

| Income | -164.4378 | 86.487 | -1.901 | 0.062 | -337.115 | 8.239 |

| dist_home_val | 1.5396 | 1.049 | 1.468 | 0.147 | -0.555 | 3.634 |

| dist_avg_income | 260.7522 | 87.058 | 2.995 | 0.004 | 86.934 | 434.570 |

| Omnibus: | 5.379 | Durbin-Watson: | 1.593 |

|---|---|---|---|

| Prob(Omnibus): | 0.068 | Jarque-Bera (JB): | 5.367 |

| Skew: | 0.642 | Prob(JB): | 0.0683 |

| Kurtosis: | 2.563 | Cond. No. | 325. |

exp.Income

0 16.03515

1 15.84750

3 11.47285

4 13.40915

5 10.03015

6 11.70575

7 11.81885

8 9.31260

9 16.28885

10 8.21290

12 10.31100

14 16.90015

15 9.81175

16 8.37990

17 9.57100

18 7.91000

22 8.36860

23 7.43320

25 6.62415

26 8.53830

27 6.67270

29 10.96410

30 7.37330

32 7.02025

34 9.13150

35 7.62235

39 6.14075

40 5.92290

41 7.93215

42 7.79915

...

56 5.91685

57 5.04755

58 3.99125

60 4.91825

61 5.66840

62 5.80935

64 5.02000

67 7.78860

68 7.30525

69 6.07935

71 4.93595

72 4.90190

73 5.15780

74 6.35895

75 5.09540

76 5.89170

78 4.81890

80 5.06555

81 4.19345

82 4.62600

83 6.42760

84 6.17745

85 5.33175

87 5.44810

89 5.22925

93 4.05520

94 3.89305

96 4.37960

97 3.49390

98 3.81590

Name: Income, Length: 70, dtype: float64

多元线性回归的变量筛选

'''forward select'''

def forward_select(data, response):

remaining = set(data.columns)

remaining.remove(response)

selected = []

current_score, best_new_score = float('inf'), float('inf')

while remaining:

aic_with_candidates=[]

for candidate in remaining:

formula = "{} ~ {}".format(

response,' + '.join(selected + [candidate]))

aic = ols(formula=formula, data=data).fit().aic

aic_with_candidates.append((aic, candidate))

aic_with_candidates.sort(reverse=True)

best_new_score, best_candidate=aic_with_candidates.pop()

if current_score > best_new_score:

remaining.remove(best_candidate)

selected.append(best_candidate)

current_score = best_new_score

print ('aic is {},continuing!'.format(current_score))

else:

print ('forward selection over!')

break

formula = "{} ~ {} ".format(response,' + '.join(selected))

print('final formula is {}'.format(formula))

model = ols(formula=formula, data=data).fit()

return(model)

data_for_select = exp[['avg_exp', 'Income', 'Age', 'dist_home_val',

'dist_avg_income']]

lm_m = forward_select(data=data_for_select, response='avg_exp')

print(lm_m.rsquared)

aic is 1007.6801413968115,continuing!

aic is 1005.4969816306302,continuing!

aic is 1005.2487355956046,continuing!

forward selection over!

final formula is avg_exp ~ dist_avg_income + Income + dist_home_val

0.541151292841195

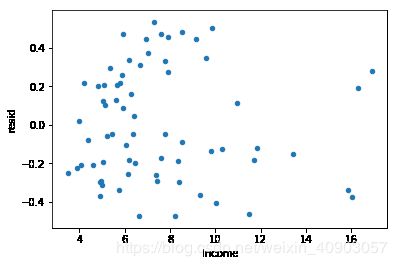

线性回归的诊断

残差分析

ana1 = lm_s

exp['Pred'] = ana1.predict(exp)

exp['resid'] = ana1.resid

exp.plot('Income', 'resid',kind='scatter')

plt.show()

[外链图片转存 (img-2JPBqa8G-1562725477554)(output_24_0.png)]

(img-2JPBqa8G-1562725477554)(output_24_0.png)]

遇到异方差情况,教科书上会介绍使用加权最小二乘法,但是实际上最常用的是对被解释变量取对数

ana2 = ols('avg_exp_ln ~ Income', exp).fit()

exp['Pred'] = ana2.predict(exp)

exp['resid'] = ana2.resid

exp.plot('Income', 'resid',kind='scatter')

plt.show()

[外链图片转存 (img-py8qc9gM-1562725477555)(output_26_0.png)]

(img-py8qc9gM-1562725477555)(output_26_0.png)]

取对数会使模型更有解释意义

exp['Income_ln'] = np.log(exp['Income'])

ana3 = ols('avg_exp_ln ~ Income_ln', exp).fit()

exp['Pred'] = ana3.predict(exp)

exp['resid'] = ana3.resid

exp.plot('Income_ln', 'resid',kind='scatter')

plt.show()

[外链图片转存 (img-ETbm7yUC-1562725477555)(output_29_0.png)]

(img-ETbm7yUC-1562725477555)(output_29_0.png)]

寻找最优的模型

r_sq = {'exp~Income':ana1.rsquared, 'ln(exp)~Income':ana2.rsquared,

'ln(exp)~ln(Income)':ana3.rsquared}

print(r_sq)

{'ln(exp)~Income': 0.4030855555329649, 'ln(exp)~ln(Income)': 0.4803927993893108, 'exp~Income': 0.45429062315565294}

强影响点分析

exp['resid_t'] = \

(exp['resid'] - exp['resid'].mean()) / exp['resid'].std()

Find outlier:

exp[abs(exp['resid_t']) > 2]

| avg_exp | avg_exp_ln | gender | Age | ... | Pred | resid | Income_ln | resid_t | |

|---|---|---|---|---|---|---|---|---|---|

| 73 | 251.56 | 5.527682 | 0 | 29 | ... | 6.526331 | -0.998649 | 1.640510 | -2.910292 |

| 98 | 163.18 | 5.094854 | 0 | 22 | ... | 6.257191 | -1.162337 | 1.339177 | -3.387317 |

2 rows × 15 columns

Drop outlier

exp2 = exp[abs(exp['resid_t']) <= 2].copy()

ana4 = ols('avg_exp_ln ~ Income_ln', exp2).fit()

exp2['Pred'] = ana4.predict(exp2)

exp2['resid'] = ana4.resid

exp2.plot('Income', 'resid', kind='scatter')

plt.show()

[外链图片转存 (img-YVNFKJRc-1562725477556)(output_37_0.png)]

(img-YVNFKJRc-1562725477556)(output_37_0.png)]

ana4.rsquared

0.49397191385172456

statemodels包提供了更多强影响点判断指标

from statsmodels.stats.outliers_influence import OLSInfluence

OLSInfluence(ana3).summary_frame().head()

| dfb_Intercept | dfb_Income_ln | cooks_d | dffits | dffits_internal | hat_diag | standard_resid | student_resid | |

|---|---|---|---|---|---|---|---|---|

| 0 | 0.343729 | -0.381393 | 0.085587 | -0.416040 | -0.413732 | 0.089498 | -1.319633 | -1.326996 |

| 1 | 0.307196 | -0.341294 | 0.069157 | -0.373146 | -0.371907 | 0.087409 | -1.201699 | -1.205702 |

| 3 | 0.207619 | -0.244956 | 0.044984 | -0.302382 | -0.299947 | 0.041557 | -1.440468 | -1.452165 |

| 4 | 0.112301 | -0.127713 | 0.010759 | -0.145967 | -0.146693 | 0.060926 | -0.575913 | -0.573062 |

| 5 | 0.120572 | -0.150924 | 0.022274 | -0.211842 | -0.211064 | 0.029011 | -1.221080 | -1.225579 |

增加变量

经过单变量线性回归的处理,我们基本对模型的性质有了一定的了解,接下来可以放入更多的连续型解释变量。在加入变量之前,要注意变量的函数形式转变。比如当地房屋均价、当地平均收入,其性质和个人收入一样,都需要取对数

exp2['dist_home_val_ln'] = np.log(exp2['dist_home_val'])

exp2['dist_avg_income_ln'] = np.log(exp2['dist_avg_income'])

ana5 = ols('''avg_exp_ln ~ Age + Income_ln +

dist_home_val_ln + dist_avg_income_ln''', exp2).fit()

ana5.summary()

| Dep. Variable: | avg_exp_ln | R-squared: | 0.553 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.525 |

| Method: | Least Squares | F-statistic: | 19.48 |

| Date: | Mon, 30 Apr 2018 | Prob (F-statistic): | 1.79e-10 |

| Time: | 16:59:34 | Log-Likelihood: | -7.3496 |

| No. Observations: | 68 | AIC: | 24.70 |

| Df Residuals: | 63 | BIC: | 35.80 |

| Df Model: | 4 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.6265 | 0.317 | 14.574 | 0.000 | 3.992 | 5.261 |

| Age | -0.0006 | 0.005 | -0.117 | 0.907 | -0.011 | 0.010 |

| Income_ln | -0.1802 | 0.569 | -0.317 | 0.752 | -1.317 | 0.957 |

| dist_home_val_ln | 0.1258 | 0.058 | 2.160 | 0.035 | 0.009 | 0.242 |

| dist_avg_income_ln | 1.0093 | 0.612 | 1.649 | 0.104 | -0.214 | 2.233 |

| Omnibus: | 4.111 | Durbin-Watson: | 1.609 |

|---|---|---|---|

| Prob(Omnibus): | 0.128 | Jarque-Bera (JB): | 2.466 |

| Skew: | 0.248 | Prob(JB): | 0.291 |

| Kurtosis: | 2.210 | Cond. No. | 807. |

多重共线性分析

# Step regression is not always work.

ana5.bse # The standard errors of the parameter estimates

Intercept 0.317453

Age 0.005124

Income_ln 0.568848

dist_home_val_ln 0.058210

dist_avg_income_ln 0.612197

dtype: float64

The function “statsmodels.stats.outliers_influence.variance_inflation_factor” uses “OLS” to fit data, and it will generates a wrong rsquared. So define it ourselves!

def vif(df, col_i):

cols = list(df.columns)

cols.remove(col_i)

cols_noti = cols

formula = col_i + '~' + '+'.join(cols_noti)

r2 = ols(formula, df).fit().rsquared

return 1. / (1. - r2)

exog = exp2[['Age', 'Income_ln', 'dist_home_val_ln',

'dist_avg_income_ln']]

for i in exog.columns:

print(i, '\t', vif(df=exog, col_i=i))

Age 1.1691185387170273

Income_ln 36.98331414029262

dist_home_val_ln 1.0536287165865763

dist_avg_income_ln 36.92286614125582

Income_ln与dist_avg_income_ln具有共线性,使用“高出平均收入的比率”代替其中一个

exp2['high_avg_ratio'] = exp2['high_avg'] / exp2['dist_avg_income']

exog1 = exp2[['Age', 'high_avg_ratio', 'dist_home_val_ln',

'dist_avg_income_ln']]

for i in exog1.columns:

print(i, '\t', vif(df=exog1, col_i=i))

Age 1.1707655829292059

high_avg_ratio 1.1347192500556706

dist_home_val_ln 1.0527329388079925

dist_avg_income_ln 1.308904149355328

var_select = exp2[['avg_exp_ln', 'Age', 'high_avg_ratio',

'dist_home_val_ln', 'dist_avg_income_ln']]

ana7 = forward_select(data=var_select, response='avg_exp_ln')

print(ana7.rsquared)

aic is 23.816793700737364,continuing!

aic is 20.83095227956072,continuing!

forward selection over!

final formula is avg_exp_ln ~ dist_avg_income_ln + dist_home_val_ln

0.5520397736845982

exp2.Ownrent

0 1

1 1

3 1

4 1

5 0

6 1

7 1

8 1

9 1

10 1

12 1

14 0

15 1

16 1

17 0

18 1

22 1

23 0

25 0

26 1

27 0

29 1

30 0

32 0

34 1

35 0

39 0

40 0

41 1

42 0

..

54 0

55 0

56 0

57 0

58 1

60 0

61 0

62 0

64 0

67 1

68 1

69 1

71 0

72 0

74 1

75 0

76 1

78 0

80 0

81 0

82 0

83 1

84 0

85 0

87 1

89 0

93 0

94 0

96 0

97 0

Name: Ownrent, Length: 68, dtype: int64

formula8 = '''

avg_exp_ln ~ dist_avg_income_ln + dist_home_val_ln +

C(gender) + C(Ownrent) + C(Selfempl) + C(edu_class)

'''

ana8 = ols(formula8, exp2).fit()

ana8.summary()

| Dep. Variable: | avg_exp_ln | R-squared: | 0.873 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.858 |

| Method: | Least Squares | F-statistic: | 58.71 |

| Date: | Mon, 30 Apr 2018 | Prob (F-statistic): | 1.75e-24 |

| Time: | 16:59:34 | Log-Likelihood: | 35.337 |

| No. Observations: | 68 | AIC: | -54.67 |

| Df Residuals: | 60 | BIC: | -36.92 |

| Df Model: | 7 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.5520 | 0.212 | 21.471 | 0.000 | 4.128 | 4.976 |

| C(gender)[T.1] | -0.4301 | 0.060 | -7.200 | 0.000 | -0.550 | -0.311 |

| C(Ownrent)[T.1] | 0.0184 | 0.045 | 0.413 | 0.681 | -0.071 | 0.107 |

| C(Selfempl)[T.1] | -0.3805 | 0.119 | -3.210 | 0.002 | -0.618 | -0.143 |

| C(edu_class)[T.2] | 0.2895 | 0.051 | 5.658 | 0.000 | 0.187 | 0.392 |

| C(edu_class)[T.3] | 0.4686 | 0.060 | 7.867 | 0.000 | 0.349 | 0.588 |

| dist_avg_income_ln | 0.9563 | 0.098 | 9.722 | 0.000 | 0.760 | 1.153 |

| dist_home_val_ln | 0.0522 | 0.034 | 1.518 | 0.134 | -0.017 | 0.121 |

| Omnibus: | 3.788 | Durbin-Watson: | 2.129 |

|---|---|---|---|

| Prob(Omnibus): | 0.150 | Jarque-Bera (JB): | 4.142 |

| Skew: | 0.020 | Prob(JB): | 0.126 |

| Kurtosis: | 4.208 | Cond. No. | 60.2 |

formula9 = '''

avg_exp_ln ~ dist_avg_income_ln + dist_home_val_ln +

C(Selfempl) + C(gender)*C(edu_class)

'''

ana9 = ols(formula9, exp2).fit()

ana9.summary()

| Dep. Variable: | avg_exp_ln | R-squared: | 0.914 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.902 |

| Method: | Least Squares | F-statistic: | 78.50 |

| Date: | Mon, 30 Apr 2018 | Prob (F-statistic): | 1.42e-28 |

| Time: | 16:59:34 | Log-Likelihood: | 48.743 |

| No. Observations: | 68 | AIC: | -79.49 |

| Df Residuals: | 59 | BIC: | -59.51 |

| Df Model: | 8 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 4.4098 | 0.178 | 24.839 | 0.000 | 4.055 | 4.765 |

| C(Selfempl)[T.1] | -0.2945 | 0.101 | -2.908 | 0.005 | -0.497 | -0.092 |

| C(gender)[T.1] | -0.0054 | 0.098 | -0.055 | 0.956 | -0.201 | 0.190 |

| C(edu_class)[T.2] | 0.3164 | 0.045 | 7.012 | 0.000 | 0.226 | 0.407 |

| C(edu_class)[T.3] | 0.5576 | 0.054 | 10.268 | 0.000 | 0.449 | 0.666 |

| C(gender)[T.1]:C(edu_class)[T.2] | -0.4304 | 0.111 | -3.865 | 0.000 | -0.653 | -0.208 |

| C(gender)[T.1]:C(edu_class)[T.3] | -0.5948 | 0.111 | -5.362 | 0.000 | -0.817 | -0.373 |

| dist_avg_income_ln | 0.9893 | 0.078 | 12.700 | 0.000 | 0.833 | 1.145 |

| dist_home_val_ln | 0.0654 | 0.029 | 2.278 | 0.026 | 0.008 | 0.123 |

| Omnibus: | 5.023 | Durbin-Watson: | 1.722 |

|---|---|---|---|

| Prob(Omnibus): | 0.081 | Jarque-Bera (JB): | 5.070 |

| Skew: | -0.328 | Prob(JB): | 0.0793 |

| Kurtosis: | 4.166 | Cond. No. | 61.1 |

正则算法

岭回归

exp.columns

Index(['avg_exp', 'avg_exp_ln', 'gender', 'Age', 'Income', 'Ownrent',

'Selfempl', 'dist_home_val', 'dist_avg_income', 'high_avg', 'edu_class',

'Pred', 'resid', 'Income_ln', 'resid_t'],

dtype='object')

lmr = ols('avg_exp ~ Income + dist_home_val + dist_avg_income',

data=exp).fit_regularized(alpha=1, L1_wt=0)

# print(lmr.summary2())

# L1_wt参数为0则使用岭回归,为1使用lasso

lmr.predict(exp_new)

lmr.summary()

LASSO算法

lmr1 = ols('avg_exp ~ Age + Income + dist_home_val + dist_avg_income',

data=exp).fit_regularized(alpha=1, L1_wt=1)

lmr1.summary()

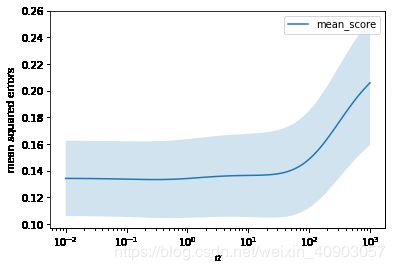

使用scikit-learn进行正则化参数调优

from sklearn.preprocessing import StandardScaler

continuous_xcols = ['Age', 'Income', 'dist_home_val',

'dist_avg_income'] # 抽取连续变量

scaler = StandardScaler() # 标准化

X = scaler.fit_transform(exp[continuous_xcols])

y = exp['avg_exp_ln']

from sklearn.linear_model import RidgeCV

alphas = np.logspace(-2, 3, 100, base=10)

# Search the min MSE by CV

rcv = RidgeCV(alphas=alphas, store_cv_values=True)

rcv.fit(X, y)

RidgeCV(alphas=array([1.00000e-02, 1.12332e-02, ..., 8.90215e+02, 1.00000e+03]),

cv=None, fit_intercept=True, gcv_mode=None, normalize=False,

scoring=None, store_cv_values=True)

print('The best alpha is {}'.format(rcv.alpha_))

print('The r-square is {}'.format(rcv.score(X, y)))

# Default score is rsquared

The best alpha is 0.2915053062825176

The r-square is 0.47568267770195016

X_new = scaler.transform(exp_new[continuous_xcols])

np.exp(rcv.predict(X_new)[:5])

array([759.67677561, 606.74024213, 661.20654568, 681.888929 ,

641.06967182])

cv_values = rcv.cv_values_

n_fold, n_alphas = cv_values.shape

cv_mean = cv_values.mean(axis=0)

cv_std = cv_values.std(axis=0)

ub = cv_mean + cv_std / np.sqrt(n_fold)

lb = cv_mean - cv_std / np.sqrt(n_fold)

plt.semilogx(alphas, cv_mean, label='mean_score')

plt.fill_between(alphas, lb, ub, alpha=0.2)

plt.xlabel("$\\alpha$")

plt.ylabel("mean squared errors")

plt.legend(loc="best")

plt.show()

[外链图片转存 (img-KBgDxHs6-1562725477557)(output_66_0.png)]

(img-KBgDxHs6-1562725477557)(output_66_0.png)]

rcv.coef_

array([ 0.03321449, -0.30956185, 0.05551208, 0.59067449])

手动选择正则化系数——根据业务判断

岭迹图

from sklearn.linear_model import Ridge

ridge = Ridge()

coefs = []

for alpha in alphas:

ridge.set_params(alpha=alpha)

ridge.fit(X, y)

coefs.append(ridge.coef_)

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Ridge coefficients as a function of the regularization')

plt.axis('tight')

plt.show()

[外链图片转存 (img-SOMLQtO1-1562725477557)(output_71_0.png)]

(img-SOMLQtO1-1562725477557)(output_71_0.png)]

ridge.set_params(alpha=0.29)

ridge.fit(X, y)

ridge.coef_

array([ 0.03322236, -0.31025822, 0.05550095, 0.59137388])

ridge.score(X, y)

0.45063153541700307

预测

np.exp(ridge.predict(X_new)[:5])

array([934.79025945, 727.11042209, 703.88143602, 759.04342764,

709.54172995])

lasso

from sklearn.linear_model import LassoCV

lasso_alphas = np.logspace(-3, 0, 100, base=10)

lcv = LassoCV(alphas=lasso_alphas, cv=10) # Search the min MSE by CV

lcv.fit(X, y)

print('The best alpha is {}'.format(lcv.alpha_))

print('The r-square is {}'.format(lcv.score(X, y)))

# Default score is rsquared

The best alpha is 0.04037017258596556

The r-square is 0.4426451069862233

from sklearn.linear_model import Lasso

lasso = Lasso()

lasso_coefs = []

for alpha in lasso_alphas:

lasso.set_params(alpha=alpha)

lasso.fit(X, y)

lasso_coefs.append(lasso.coef_)

ax = plt.gca()

ax.plot(lasso_alphas, lasso_coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Lasso coefficients as a function of the regularization')

plt.axis('tight')

plt.show()

[外链图片转存 (img-rdcRKGfS-1562725477558)(output_79_0.png)]

(img-rdcRKGfS-1562725477558)(output_79_0.png)]

lcv.coef_

array([0. , 0. , 0.02789489, 0.26549855])

弹性网络

from sklearn.linear_model import ElasticNetCV

l1_ratio = [0.01, .1, .5, .7, .9, .95, .99, 1]

encv = ElasticNetCV(l1_ratio=l1_ratio)

encv.fit(X, y)

ElasticNetCV(alphas=None, copy_X=True, cv=None, eps=0.001, fit_intercept=True,

l1_ratio=[0.01, 0.1, 0.5, 0.7, 0.9, 0.95, 0.99, 1], max_iter=1000,

n_alphas=100, n_jobs=1, normalize=False, positive=False,

precompute='auto', random_state=None, selection='cyclic',

tol=0.0001, verbose=0)

print('The best l1_ratio is {}'.format(encv.l1_ratio_))

print('The best alpha is {}'.format(encv.alpha_))

The best l1_ratio is 0.01

The best alpha is 1.0998728529638144