GARCH模型案例分析

read data

library(quantmod) # 加载包

getSymbols('^HSI', from='1989-12-01',to='2013-11-30') # 从Yahoo网站下载恒生指数日价格数据

dim(HSI) # 数据规模

names(HSI) # 数据变量名称

chartSeries(HSI,theme='white') # 画出价格与交易的时序图

HSI <-read.table('HSI.txt') # 或者从硬盘中读取恒生指数日价格数据

HSI <-as.xts(HSI) # 将数据格式转化为xts格式

compute return series

ptd.HSI <-HSI$HSI.Adjusted # 提取日收盘价信息

rtd.HSI <-diff(log(ptd.HSI))*100 # 计算日对数收益

rtd.HSI <-rtd.HSI[-1,] # 删除一期缺失值

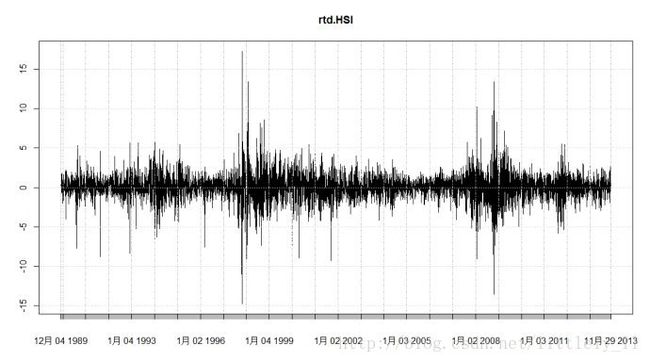

plot(rtd.HSI) # 画出日收益序列的时序图

![]()

ptm.HSI <-to.monthly(HSI)$HSI.Adjusted # 提取月收盘价信息

rtm.HSI <-diff(log(ptm.HSI))*100 # 计算月对数收益

rtm.HSI <-rtm.HSI[-1,] # 删除一期缺失值

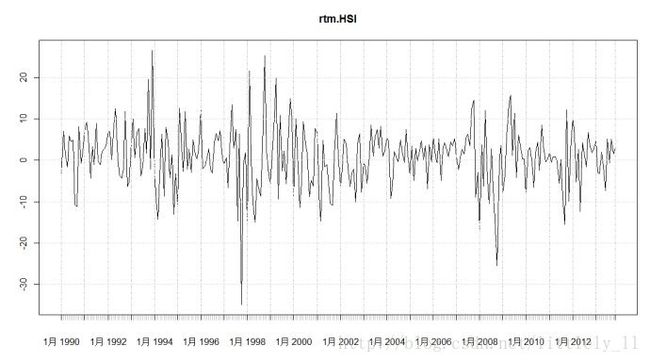

plot(rtm.HSI) # 画出月收益序列的时序图

detach(package:quantmod)

ARCH效应检验

# rtm.HSI <- as.numeric(rtm.HSI)

ind.outsample <- sub(' ','',substr(index(rtm.HSI), 4, 8)) %in%'2013' #设置样本外下标:2013年为样本外

ind.insample <-!ind.outsample # 设置样本内下标:其余为样本内

rtm.insample <- rtm.HSI[ind.insample]

rtm.outsample <- rtm.HSI[ind.outsample]

Box.test(rtm.insample, lag=12,type='Ljung-Box') # 月收益序列不存在自相关

Box.test(rtm.insample^2, lag=12,type='Ljung-Box') # 平方月收益序列存在自相关

FinTS::ArchTest(x=rtm.insample,lags=12) # 存在显著的ARCH效应

模型定阶

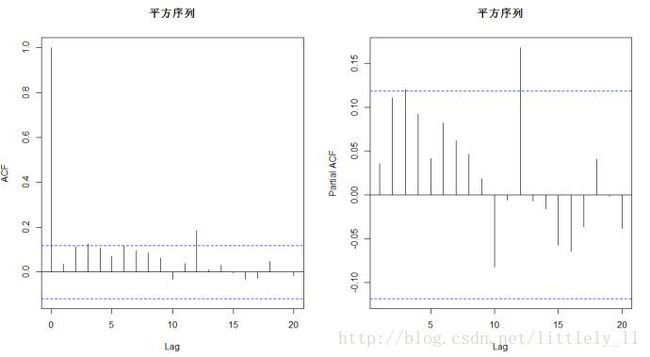

epst <- rtm.insample -mean(rtm.insample) # 均值调整对数收益

par(mfrow=c(1,2))

acf(as.numeric(epst)^2, lag.max=20, main='平方序列')

pacf(as.numeric(epst)^2, lag.max=20,main='平方序列')

建立GARCH类模型

library(fGarch)

GARCH.model_1 <- garchFit(~garch(1,1), data=rtm.insample,trace=FALSE) # GARCH(1,1)-N模型

GARCH.model_2 <- garchFit(~garch(2,1), data=rtm.insample,trace=FALSE) # GARCH(1,2)-N模型

GARCH.model_3 <- garchFit(~garch(1,1), data=rtm.insample,cond.dist='std', trace=FALSE) #GARCH(1,1)-t模型

GARCH.model_4 <- garchFit(~garch(1,1), data=rtm.insample,cond.dist='sstd', trace=FALSE) #GARCH(1,1)-st模型

GARCH.model_5 <- garchFit(~garch(1,1), data=rtm.insample,cond.dist='ged', trace=FALSE) #GARCH(1,1)-GED模型

GARCH.model_6 <- garchFit(~garch(1,1), data=rtm.insample,cond.dist='sged', trace=FALSE) #GARCH(1,1)-SGED模型

summary(GARCH.model_1)

summary(GARCH.model_3)

plot(GARCH.model_1)提取GARCH类模型信息

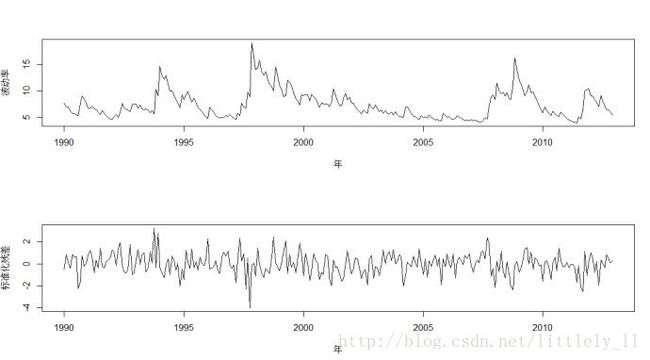

vol_1 <-fBasics::volatility(GARCH.model_1) # 提取GARCH(1,1)-N模型得到的波动率估计

sres_1 <- residuals(GARCH.model_1,standardize=TRUE) # 提取GARCH(1,1)-N模型得到的标准化残差

vol_1.ts <- ts(vol_1, frequency=12, start=c(1990, 1))

sres_1.ts <- ts(sres_1, frequency=12, start=c(1990, 1))

par(mfcol=c(2,1))

plot(vol_1.ts, xlab='年', ylab='波动率')

plot(sres_1.ts, xlab='年', ylab='标准化残差')

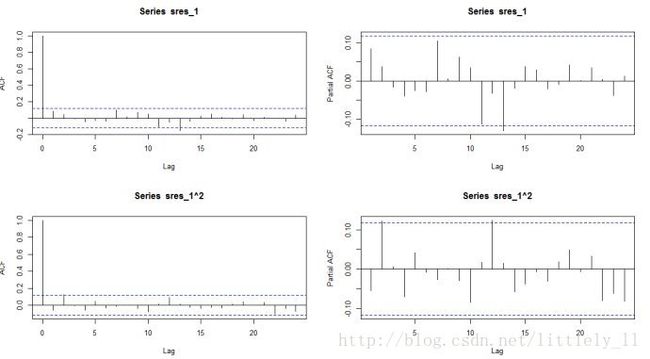

模型检验

par(mfrow=c(2,2))

acf(sres_1, lag=24)

pacf(sres_1, lag=24)

acf(sres_1^2, lag=24)

pacf(sres_1^2, lag=24)![]()

par(mfrow=c(1,1))

qqnorm(sres_1)

qqline(sres_1)

模型预测

pred.model_1 <- predict(GARCH.model_1, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

pred.model_2 <- predict(GARCH.model_2, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

pred.model_3 <- predict(GARCH.model_3, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

pred.model_4 <- predict(GARCH.model_4, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

pred.model_5 <- predict(GARCH.model_5, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

pred.model_6 <- predict(GARCH.model_6, n.ahead = 11, trace =FALSE, mse = 'cond', plot=FALSE)

predVol_1 <-pred.model_1$standardDeviation

predVol_2 <- pred.model_2$standardDeviation

predVol_3 <- pred.model_3$standardDeviation

predVol_4 <- pred.model_4$standardDeviation

predVol_5 <- pred.model_5$standardDeviation

predVol_6 <- pred.model_6$standardDeviation

et <- abs(rtm.outsample - mean(rtm.outsample))

rtd.HSI.2013 <- rtd.HSI['2013']

rv <- sqrt(aggregate(rtd.HSI.2013^2,by=substr(index(rtd.HSI.2013), 1, 7), sum))

predVol <-round(rbind(predVol_1,predVol_2,predVol_3,predVol_4,predVol_5,predVol_6,

as.numeric(et), as.numeric(rv)), digits=3)

colnames(predVol) <- 1:11

rownames(predVol) <-c('GARCH(1,1)-N模型','GARCH(1,2)-N模型','GARCH(1,1)-t模型','GARCH(1,1)-st模型','GARCH(1,1)-GED模型','GARCH(1,1)-SGED模型','残差绝对值', '已实现波动')

print(predVol) 1 2 3 4 5 6 7 8 9 10 11

GARCH(1,1)-N模型 5.037 5.286 5.513 5.722 5.915 6.094 6.260 6.415 6.560 6.696 6.824

GARCH(1,2)-N模型 4.760 4.747 5.136 5.404 5.661 5.891 6.102 6.296 6.473 6.638 6.789

GARCH(1,1)-t模型 5.347 5.532 5.703 5.864 6.014 6.154 6.286 6.410 6.527 6.638 6.742

GARCH(1,1)-st模型 5.386 5.560 5.722 5.873 6.014 6.146 6.270 6.386 6.495 6.598 6.695

GARCH(1,1)-GED模型 5.168 5.374 5.565 5.741 5.906 6.059 6.203 6.338 6.464 6.583 6.695

GARCH(1,1)-SGED模型 5.229 5.423 5.601 5.767 5.920 6.063 6.197 6.322 6.439 6.548 6.651

残差绝对值 4.147 3.513 3.659 1.464 2.007 7.838 4.584 1.177 4.584 1.026 2.388已实现波动 3.543 4.114 3.929 4.778 4.374 6.013 5.397 4.634 4.070 3.745 4.395模型选择

cor(t(predVol))