金融风控-贷款违约预测学习笔记(Part4:建模与超参调整)

金融风控-贷款违约预测学习笔记(Part4:建模与超参调整)

- 1. 模型与其相关原理介绍

- 2. 模型对比与性能评估

-

- 2.2 逻辑回归

- 2.3 决策树模型

- 2.4 集成学习方法

- 3. 模型评估方法

-

- 3.1 留出法

- 3.2 交叉验证法

- 3.3 自助法

- 3.4 总结:

- 4. 模型评价标准

- 5. 代码示例

-

- 5.1 模块导入

- 5.2 读取数据

- 5.3 简单建模

- 5.4 模型调参

-

- 5.4.1 贪心调参

- 5.4.2 网格搜索

- 5.4.3 贝叶斯调参

- 5.5 建立最终模型

本节主要内容:模型创建,模型评价和调参策略

资料参考:https://github.com/datawhalechina/team-learning-data-mining/blob/master/FinancialRiskControl/Task4%20%E5%BB%BA%E6%A8%A1%E8%B0%83%E5%8F%82.md

1. 模型与其相关原理介绍

参考资料

-

1 逻辑回归模型

https://blog.csdn.net/han_xiaoyang/article/details/49123419 -

2 决策树模型

https://blog.csdn.net/c406495762/article/details/76262487 -

3 GBDT模型

https://zhuanlan.zhihu.com/p/45145899 -

4 XGBoost模型

https://blog.csdn.net/wuzhongqiang/article/details/104854890 -

5 LightGBM模型

https://blog.csdn.net/wuzhongqiang/article/details/105350579 -

6 Catboost模型

https://mp.weixin.qq.com/s/xloTLr5NJBgBspMQtxPoFA -

7 时间序列模型)

RNN:https://zhuanlan.zhihu.com/p/45289691

LSTM:https://zhuanlan.zhihu.com/p/83496936

-

8 推荐教材:

《机器学习》 https://book.douban.com/subject/26708119/

《统计学习方法》 https://book.douban.com/subject/10590856/

《面向机器学习的特征工程》 https://book.douban.com/subject/26826639/

《信用评分模型技术与应用》https://book.douban.com/subject/1488075/

《数据化风控》https://book.douban.com/subject/30282558/

2. 模型对比与性能评估

2.2 逻辑回归

- 训练速度快,简单易理解,可解释性强

- 需要分箱、归一化、处理异常值和缺失值

虽然可以引入非线性项来解决非线性问题,但是效果不佳

2.3 决策树模型

- 不需要预处理,不需要归一化,不需要处理缺失数据

- 采用贪心算法,容易得到局部最优解。

2.4 集成学习方法

常见的有bagging、boosting、stacking等,都是将已有的分类或回归算法通过一定方式组合起来,形成一个更加强大的分类器,区别在于结合方式不一样。

3. 模型评估方法

3.1 留出法

将数据集划分为训练集和测试集,且划分的时候要尽可能保证数据分布的一致性(这里的数据分布是否指目标特征的分布?)。为保证数据分布的一致性,通常采用分层采样的方式来对数据集进行采样。

3.2 交叉验证法

k折交叉验证法,通常将数据集分为K份,

交叉验证中数据集的划分依然是依据分层采样的方式来进行

3.3 自助法

对数据集进行m次的有放回抽样,得到大小为m的训练集。因为是有放回抽样,所以有的样本没有被重复抽取,有的样本则未被抽取。未被抽取的样本作为测试。

3.4 总结:

- 数据集样本量充足时,可以采用留出法和K折交叉验证法

- 数据集样本量小,且难以有效划分训练/测试集的时候,使用自助法

- 数据集样本量小,且可以有效划分训练/测试集的时候,最好使用留一法

4. 模型评价标准

本次竞赛中,以AUC作为模型评价标准。详见Part1:赛题理解

5. 代码示例

5.1 模块导入

import pandas as pd

import numpy as np

import warnings

import os

import seaborn as sns

import matplotlib.pyplot as plt

c:\users\honk\appdata\local\programs\python\python37\lib\site-packages\statsmodels\tools\_testing.py:19: FutureWarning: pandas.util.testing is deprecated. Use the functions in the public API at pandas.testing instead.

import pandas.util.testing as tm

"""

seaborn 相关设置

"""

# 将matplotlib的图表样式替换成seaborn的图标样式

sns.set()

# 设定绘图风格。可选参数值:darkgrid(默认), whitegrid, dark, white, ticks

sns.set_style('whitegrid')

# 绘图元素比例。可选参数值(线条和字体越来越粗):paper,notebook(默认),talk,poster

sns.set_context('talk')

# 中文字体设置,解决中文字体无法显示的问题

plt.rcParams['font.sans-serif'] = ['SimHei']

sns.set(font='SimHei')

# 解决负号'-'无法正常显示的问题

plt.rcParams['axes.unicode_minus'] = False

5.2 读取数据

def reduce_mem_usage(df):

# 调整之前的内存占用空间 (返回的单位是byte)

start_mem = df.memory_usage().sum()

print('Memory usage of dataframe is {:.2f} MB'.format(start_mem))

for col in df.columns:

col_dtype = df[col].dtype

if col_dtype != object:

c_min = df[col].min()

c_max = df[col].max()

if str(col_dtype)[:3] == 'int':

for dtype in [np.int8, np.int16, np.int32, np.int64]:

if c_min > np.iinfo(dtype).min and c_max < np.iinfo(dtype).max:

df[col] = df[col].astype(dtype)

break

else:

for dtype in [np.float16, np.float32, np.float64]:

if c_min > np.finfo(dtype).min and c_max < np.finfo(dtype).max:

df[col] = df[col].astype(dtype)

break

else:

df[col] = df[col].astype('category')

end_mem = df.memory_usage().sum()

print('Memory usage after optimization is: {:.2f}MB'.format(end_mem))

print('Decreased by {:.1f}%'.format(100 * (start_mem - end_mem)/start_mem))

return df

x_train = pd.read_csv('Dataset/data_for_model.csv')

x_train = reduce_mem_usage(x_train)

y_train = pd.read_csv('Dataset/label_for_model.csv')['isDefault'].astype(np.int8)

Memory usage of dataframe is 377449200.00 MB

Memory usage after optimization is: 92524170.00MB

Decreased by 75.5%

5.3 简单建模

使用Lightgbm进行建模

"""

对训练集数据进行划分,分成训练集和验证集,并进行相应的操作

"""

from sklearn.model_selection import train_test_split

import lightgbm as lgb

# 数据集划分

X_train_split, X_val, y_train_split, y_val = train_test_split(x_train, y_train, test_size=0.2)

train_matrix = lgb.Dataset(X_train_split, label=y_train_split)

valid_matrix = lgb.Dataset(X_val, label=y_val)

params = {

'boosting_type': 'gbdt',

'objective': 'binary',

'learning_rate': 0.1,

'metric': 'auc',

'min_child_weight': 1e-3,

'num_leaves': 31,

'max_depth': -1,

'reg_lambda': 0,

'reg_alpha': 0,

'feature_fraction': 1,

'bagging_fraction': 1,

'bagging_freq': 0,

'seed': 2020,

'nthread': 8,

'silent': True,

'verbose': -1

}

"""

使用训练集数据进行模型训练

"""

model = lgb.train(params, train_set=train_matrix, valid_sets=valid_matrix,

num_boost_round=20000, verbose_eval=1000, early_stopping_rounds=200)

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[334] valid_0's auc: 0.729254

对验证集进行预测

from sklearn import metrics

from sklearn.metrics import roc_auc_score

"""

预测并计算roc的相关指标

"""

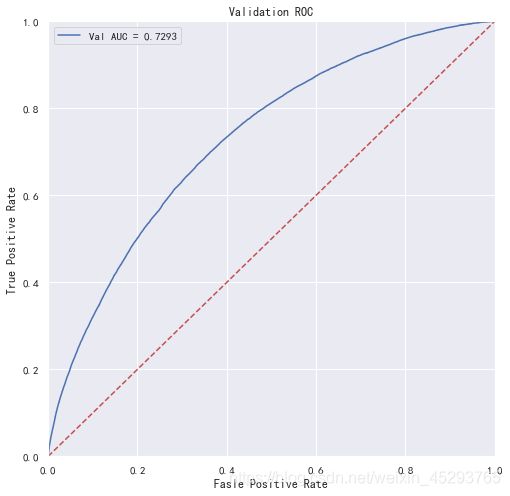

val_pre_lgb = model.predict(X_val, num_iteration=model.best_iteration)

fpr, tpr, threshold = metrics.roc_curve(y_val, val_pre_lgb)

roc_auc = metrics.auc(fpr, tpr)

print('未调参前lightgbm单模型在验证集上的AUC:{}'.format(roc_auc))

"画出roc曲线图"

plt.figure(figsize=(8, 8))

plt.title('Validation ROC')

plt.plot(fpr, tpr, 'b', label='Val AUC = %.4f' % roc_auc)

plt.ylim(0, 1)

plt.xlim(0, 1)

plt.legend(loc='best')

# plt.title('ROC')

plt.ylabel('True Positive Rate')

plt.xlabel('Fasle Positive Rate')

"画出对角线"

plt.plot([0, 1], [0, 1], 'r--')

plt.show()

未调参前lightgbm单模型在验证集上的AUC:0.7292540914716458

进一步地,使用5折交叉验证进行模型性能评估

from sklearn.model_selection import KFold

# 5折交叉验证

folds = 5

seed = 2020

kf = KFold(n_splits=folds, shuffle=True, random_state=seed)

params = {

'boosting_type': 'gbdt',

'objective': 'binary',

'learning_rate': 0.1,

'metric': 'auc',

'min_child_weight': 1e-3,

'num_leaves': 31,

'max_depth': -1,

'reg_lambda': 0,

'reg_alpha': 0,

'feature_fraction': 1,

'bagging_fraction': 1,

'bagging_freq': 0,

'seed': seed,

'nthread': 8,

'silent': True,

'verbose': -1

}

cv_scores = []

for i,(train_index, valid_index) in enumerate(kf.split(x_train, y_train)):

print('*'*30, str(i+1), '*'*30)

X_train_split, y_train_split, X_val, y_val = (x_train.iloc[train_index],

y_train.iloc[train_index],

x_train.iloc[valid_index],

y_train.iloc[valid_index])

train_matrix = lgb.Dataset(X_train_split, label=y_train_split)

valid_matrix = lgb.Dataset(X_val, label=y_val)

model = lgb.train(params, train_set=train_matrix, valid_sets=valid_matrix,

num_boost_round=20000, verbose_eval=1000, early_stopping_rounds=200)

val_pred = model.predict(X_val, num_iteration=model.best_iteration)

cv_scores.append(roc_auc_score(y_val, val_pred))

print(cv_scores)

print('lgb_scotrainre_list: ', cv_scores)

print('lgb_score_mean: ', np.mean(cv_scores))

print('lgb_score_std: ', np.std(cv_scores))

****************************** 1 ******************************

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[391] valid_0's auc: 0.729003

[0.7290028273076175]

****************************** 2 ******************************

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[271] valid_0's auc: 0.730727

[0.7290028273076175, 0.7307267609075013]

****************************** 3 ******************************

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[432] valid_0's auc: 0.731958

[0.7290028273076175, 0.7307267609075013, 0.731958201378707]

****************************** 4 ******************************

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[299] valid_0's auc: 0.727204

[0.7290028273076175, 0.7307267609075013, 0.731958201378707, 0.7272042210402802]

****************************** 5 ******************************

Training until validation scores don't improve for 200 rounds

Early stopping, best iteration is:

[287] valid_0's auc: 0.732224

[0.7290028273076175, 0.7307267609075013, 0.731958201378707, 0.7272042210402802, 0.7322240919782057]

lgb_scotrainre_list: [0.7290028273076175, 0.7307267609075013, 0.731958201378707, 0.7272042210402802, 0.7322240919782057]

lgb_score_mean: 0.7302232205224624

lgb_score_std: 0.0018905510067472465

5.4 模型调参

5.4.1 贪心调参

先使用当前对模型影响最大的参数进行调优,达到当前参数下的模型最优化,再使用对模型影响次之的参数进行调优,如此下去,直到所有的参数调整完毕。

这个方法的缺点就是可能会调到局部最优而不是全局最优,但是只需要一步一步的进行参数最优化调试即可,容易理解。

需要注意的是在树模型中参数调整的顺序,也就是各个参数对模型的影响程度,这里列举一下日常调参过程中常用的参数和调参顺序:

①:max_depth(树模型深度)、num_leaves(叶子节点数,树模型复杂度)

②:min_data_in_leaf(一个叶子上最小数据量,可以用来处理过拟合)、min_child_weight(决定最小叶子节点样本权重和。当它的值较大时,可以避免模型学习到局部的特殊样本。但如果这个值过高,会导致欠拟合。)

③:bagging_fraction(不进行重采样的情况下随机选择部分数据)、 feature_fraction(每次迭代中随机选择特征的比例)、bagging_freq(bagging的次数)

④:reg_lambda(权重的L2正则化项)、reg_alpha(权重的L1正则化项)

⑤:min_split_gain(执行切分的最小增益)

objective 可选参数值详见:https://github.com/Microsoft/LightGBM/blob/master/docs/Parameters.rst#objective

from sklearn.model_selection import cross_val_score

best_obj = dict()

objective = ['regression', 'rgression_l1', 'binary', 'cross_entropy', 'cross_entropy_lambda']

for obj in objective:

model = lgb.LGBMRegressor(objective=obj)

score = cross_val_score(model, x_train, y_train, cv=5, scoring='roc_auc').mean()

best_obj[obj] =score

best_leaves = dict()

num_leaves = range(10,80)

for leaves in num_leaves:

model = lgb.LGBMRegressor(objective=min(best_obj.items(), key=lambda x: x[1])[0],

num_leaves=leaves)

score = cross_val_score(model, x_train, y_train, cv=5, scoring='roc_auc').mean()

best_leaves[leaves] = score

best_depth = dict()

max_depth = range(3, 10)

for depth in max_depth:

model = lgb.LGBMRegressor(objective=min(best_obj.items(), key=lambad x: x[1])[0],

num_leaves=min(best_leaves.items(), key=lambad x: x[1])[0],

max_depth=depth)

score = cross_val_score(model, x_train, y_train, cv=5, scoring='roc_auc').mean()

best_depth[depth] = score

5.4.2 网格搜索

相比贪心调参效果更优。但是时间开销大,一旦数据量过大,就很难得出结果。

from sklearn.model_selection import GridSearchCV, StratifiedKFold

def get_best_cv_params(learning_rate=0.1, n_estimators=581,

num_leaves=31, max_depth=-1, bagging_fraction=1.0,

feature_fraction=1.0, bagging_req=0, min_data_in_leaf=20,

min_child_weight=0.001, min_split_gain=0, reg_lambda=0,

reg_alpha=0, param_grid=None):

cv_fold = StratifiedKFold(n_splits=5, random_state=0, shuffle=True)

model_lgb = lgb.LGBMClassifier(learning_rate=learning_rate,

n_estimators=n_estimators,

num_leaves=num_leaves,

max_depth=max_depth,

bagging_fraction=bagging_fraction,

feature_fraction=feature_fraction,

bagging_req=bagging_req,

min_data_in_leaf=min_data_in_leaf,

min_child_weight=min_child_weight,

min_split_gain=min_split_gain,

reg_lambda=reg_lambda,

reg_alpha=reg_alpha,

n_jobs=8

)

grid_searh = GridSearchCV(estimator=model_lgb,

cv=cv_fold,

param_grid=param_grid,

scoring='roc_auc'

)

grid_searh.fit(x_train, y_train)

print('模型当前最优参数为:', grid_searh.best_parmas_)

print('模型当前最优得分为:', grid_searh.best_score_)

"""以下代码未运行,耗时较长,请谨慎运行,且每一步的最优参数需要在下一步进行手动更新,请注意"""

"""

需要注意一下的是,除了获取上面的获取num_boost_round时候用的是原生的lightgbm(因为要用自带的cv)

下面配合GridSearchCV时必须使用sklearn接口的lightgbm。

"""

#设置n_estimators 为581,调整num_leaves和max_depth,这里选择先粗调再细调

lgb_params = {'num_leaves': range(10, 80, 5), 'max_depth': range(3, 10, 2)}

get_best_cv_params(learning_rate=0.1, n_estimators=581, num_leaves=None, max_depth=None,

min_data_in_leaf=20, min_child_weight=0.001, bagging_fraction=1.0,

feature_fraction=1.0, bagging_req=0, min_split_gain=0, reg_lambda=0,

reg_alpha=0, param_grid=lgb_params)

# num_leaves为30,max_depth为7,进一步细调num_leaves和max_depth

lgb_params = {'num_leaves': range(25, 35, 1), 'max_depth': range(5, 9, 1)}

get_best_cv_params(learning_rate=0.1, n_estimators=85, num_leaves=None, max_depth=None,

min_data_in_leaf=20, min_child_weight=0.001, bagging_fraction=1.0,

feature_fraction=1.0, bagging_req=1.0, min_split_gain=0,

reg_lambda=0, reg_lambda=0, reg_alpha=0, param_grid=lgb_params)

# 确定min_data_in_leaf为45,min_child_weight为0.001

# 再进行bagging_fraction、feature_fraction和bagging_freq的调参

lgb_params = {'reg_lambda': [i/10 for i in range(5, 10, 1)],

'reg_alpha': [i/10 for i in range(5, 10, 1)],

'bagging_freq': range(0, 81, 10)}

get_best_cv_params(learning_rate=0.1, n_estimators=85, num_leaves=29, max_depth=7,

min_data_in_leaf=45, min_child_weight=0.001, bagging_fraction=None,

feature_fraction=None, bagging_req=None, min_split_gain=0,

reg_lambda=0, reg_lambda=0, param_grid=lgb_params)

# 确定bagging_fraction为0.4、feature_fraction为0.6、bagging_freq为

# 再进行reg_lambda、reg_alpha的调参

lgb_params = {'reg_lambda': [0, 0.001, 0.01, 0.03, 0.08, 0.3, 0.5],

'reg_alpha': [0, 0.001, 0.01, 0.03, 0.08, 0.3, 0.5]}

get_best_cv_params(learning_rate=0.1, n_estimators=85, num_leaves=29, max_depth=7,

min_data_in_leaf=45, min_child_weight=0.001, bagging_fraction=0.9,

feature_fraction=0.9, bagging_req=40, min_split_gain=0,

reg_lambda=None, reg_lambda=None, param_grid=lgb_params)

# 确定reg_lambda、reg_alpha都为0

# 再进行min_split_gain的调参

lgb_params = {'min_split_gain': [i/10 for i in range(0, 11, 1)]}

get_best_cv_params(learning_rate=0.1, n_estimators=85, num_leaves=29, max_depth=7,

min_data_in_leaf=45, min_child_weight=0.001, bagging_fraction=0.9,

feature_fraction=0.9, bagging_req=40, min_split_gain=0,

reg_lambda=None, reg_lambda=None, param_grid=lgb_params)

"通过网格搜索确定最优参数"

final_parmas = {'boosting_type': 'gbdt',

'learning_rate': 0.01,

'num_leaves': 29,

'max_depth': 7,

'min_data_in_leaf': 45,

'min_child_weight': 0.001,

'bagging_fraction': 0.9,

'feature_fraction': 0.9,

'bagging_freq': 40,

'min_split_gain': 0,

'reg_lambda': 0,

'reg_alpha': 0,

'nthread': 6

}

cv_result = lgb.cv(train_set=lgb_train,

early_stopping_rounds=20,

num_boost_round=5000,

nfold=5,

stratified=True,

params=final_parmas,

metrics='auc',

seed=2020)

print('迭代次数: ', len(cv_result['auc-mean']))

print('交叉验证的AUC为:', max(cv_result['auc-mean']))

5.4.3 贝叶斯调参

贝叶斯调参的主要思想是:给定优化的目标函数(广义的函数,只需指定输入和输出即可,无需知道内部结构以及数学性质),通过不断地添加样本点来更新目标函数的后验分布(高斯过程,直到后验分布基本贴合于真实分布)。简单的说,就是考虑了上一次参数的信息,从而更好的调整当前的参数。

贝叶斯调参的步骤如下:

- 定义优化函数(rf_cv)

- 建立模型

- 定义待优化的参数

- 得到优化结果,并返回要优化的分数指标

# pip install bayesian-optimization

from sklearn.model_selection import cross_val_score

def rf_cv_lgb(num_leaves, max_depth, bagging_fraction, feature_fraction, bagging_freq,

min_data_in_leaf, min_child_weight, min_split_gain, reg_lambda, reg_alpha):

model_lgb = lgb.LGBMClassifier(boosting_type='gbdt', objective='binary', metric='auc',

learning_rate=0.1, n_estimators=5000, num_leaves=int(num_leaves),

max_depth=int(max_depth), bagging_fraction=round(bagging_fraction, 2),

feature_fraction=round(feature_fraction, 2), bagging_freq=int(bagging_freq),

min_data_in_leaf=int(min_data_in_leaf), min_child_weight=min_child_weight,

min_split_gain=min_split_gain, reg_lambda=reg_lambda, reg_alpha=reg_alpha,

n_jobs=8)

val = cross_val_score(model_lgb, X_train_split, y_train_split, cv=5, scoring='roc_auc').mean()

return val

from bayes_opt import BayesianOptimization

"定义需要优化的参数"

bayes_lgb = BayesianOptimization(rf_cv_lgb,

{

'num_leaves': (10, 200),

'max_depth': (3, 20),

'bagging_fraction': (0.5, 1.0),

'feature_fraction': (0.5, 1.0),

'bagging_freq': (0, 100),

'min_data_in_leaf': (10, 100),

'min_child_weight': (0, 10),

'min_split_gain': (0.0, 1.0),

'reg_alpha': (0.0, 10),

'reg_lambda': (0.0, 10)

}

)

"开始优化"

bayes_lgb.maximize(n_iter=10)

| iter | target | baggin... | baggin... | featur... | max_depth | min_ch... | min_da... | min_sp... | num_le... | reg_alpha | reg_la... |

-------------------------------------------------------------------------------------------------------------------------------------------------

| [0m 1 [0m | [0m 0.7253 [0m | [0m 0.5085 [0m | [0m 71.31 [0m | [0m 0.8524 [0m | [0m 8.124 [0m | [0m 2.889 [0m | [0m 26.92 [0m | [0m 0.5716 [0m | [0m 81.84 [0m | [0m 4.136 [0m | [0m 6.484 [0m |

| [0m 2 [0m | [0m 0.6968 [0m | [0m 0.7396 [0m | [0m 64.17 [0m | [0m 0.9414 [0m | [0m 10.52 [0m | [0m 8.3 [0m | [0m 35.48 [0m | [0m 0.02613 [0m | [0m 176.1 [0m | [0m 6.372 [0m | [0m 8.569 [0m |

| [0m 3 [0m | [0m 0.6973 [0m | [0m 0.579 [0m | [0m 19.27 [0m | [0m 0.5447 [0m | [0m 7.248 [0m | [0m 7.272 [0m | [0m 35.98 [0m | [0m 0.09783 [0m | [0m 118.7 [0m | [0m 5.358 [0m | [0m 8.89 [0m |

---------------------------------------------------------------------------

KeyError Traceback (most recent call last)

.....

KeyboardInterrupt:

因为调参时间实在是太久了。我就给先停止了。先试试3次调参后的效果怎么样。

'显示优化结果'

bayes_lgb.max

{'target': 0.7253010419224971,

'params': {'bagging_fraction': 0.5085047041852252,

'bagging_freq': 71.30936204845294,

'feature_fraction': 0.8523779866128889,

'max_depth': 8.123528975950922,

'min_child_weight': 2.8885434024723757,

'min_data_in_leaf': 26.916059861564715,

'min_split_gain': 0.5715502339115726,

'num_leaves': 81.83531877577995,

'reg_alpha': 4.135748365864206,

'reg_lambda': 6.484350951024385}}

参数优化完成后,可以根据优化后的参数建立新的模型,降低学习率并寻找最优模型迭代次数

"调整一个较小的学习率,并通过cv函数确定当前最优的迭代次数"

base_params_lgb ={'boosting_type': 'gbdt',

'objective': 'binary',

'metric': 'auc',

'learning_rate': 0.01,

'nthread': 8,

'seed': 2020,

'silent': True,

'verbose': -1

}

for fea in bayes_lgb.max['params']:

if fea in ['num_leaves', 'max_depth', 'min_data_in_leaf', 'bagging_freq']:

base_params_lgb[fea] = int(bayes_lgb.max['params'][fea])

else:

base_params_lgb[fea] = round(bayes_lgb.max['params'][fea], 2)

cv_result_lgb = lgb.cv(train_set=train_matrix,

early_stopping_rounds=1000,

num_boost_round=20000,

nfold=5,

stratified=True,

shuffle=True,

params=base_params_lgb,

metrics='auc',

seed=2020

)

print('迭代次数:', len(cv_result_lgb['auc-mean']))

print('最终模型的AUC为:', max(cv_result_lgb['auc-mean']))

迭代次数: 2290

最终模型的AUC为: 0.7301432469182637

又跑了差不多一个小时。。。

5.5 建立最终模型

模型参数已确定,建立最终模型并对验证集进行验证

cv_scores = []

for i, (train_index, valid_index) in enumerate(kf.split(x_train, y_train)):

print('*'*30, str(i+1), '*'*30)

X_train_split, y_train_split, X_val, y_val = (x_train.iloc[train_index],

y_train.iloc[train_index],

x_train.iloc[valid_index],

y_train.iloc[valid_index])

train_matrix = lgb.Dataset(X_train_split, label=y_train_split)

valid_matrix = lgb.Dataset(X_val, label=y_val)

params = base_params_lgb

# params.pop('verbose')

# verbose_eval 每迭代多少次输出一次评估结果

model = lgb.train(params, train_set=train_matrix, valid_sets=valid_matrix,

num_boost_round=2290, verbose_eval=1000, early_stopping_rounds=200)

val_pred = model.predict(X_val, num_iteration=model.best_iteration)

cv_scores.append(roc_auc_score(y_val, val_pred))

print(cv_scores)

print('lgb_scotrainre_list: ', cv_scores)

print('lgb_score_mean: ', np.mean(cv_scores))

print('lgb_score_std: ', np.std(cv_scores))

****************************** 1 ******************************

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.728198

[2000] valid_0's auc: 0.730141

Early stopping, best iteration is:

[1995] valid_0's auc: 0.730154

[0.730154013660886]

****************************** 2 ******************************

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.730745

Early stopping, best iteration is:

[1775] valid_0's auc: 0.732416

[0.730154013660886, 0.7324162622803124]

****************************** 3 ******************************

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.731586

[2000] valid_0's auc: 0.733759

Did not meet early stopping. Best iteration is:

[2210] valid_0's auc: 0.73389

[0.730154013660886, 0.7324162622803124, 0.7338895025847298]

****************************** 4 ******************************

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.727136

[2000] valid_0's auc: 0.72886

Early stopping, best iteration is:

[1982] valid_0's auc: 0.728902

[0.730154013660886, 0.7324162622803124, 0.7338895025847298, 0.7289019419414305]

****************************** 5 ******************************

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.731454

[2000] valid_0's auc: 0.733089

Did not meet early stopping. Best iteration is:

[2286] valid_0's auc: 0.733251

[0.730154013660886, 0.7324162622803124, 0.7338895025847298, 0.7289019419414305, 0.7332511170149825]

lgb_scotrainre_list: [0.730154013660886, 0.7324162622803124, 0.7338895025847298, 0.7289019419414305, 0.7332511170149825]

lgb_score_mean: 0.7317225674964682

lgb_score_std: 0.0018936511514676447

通过5折交叉验证,可以发现模型迭代到13000次后会停止,那么在建立新模型时,可以直接设置最大迭代次数为13000,并使用验证集进行模型预测。

X_train_split, X_val, y_train_split, y_val = train_test_split(x_train, y_train, test_size=0.2)

train_matrix = lgb.Dataset(X_train_split, label=y_train_split)

valid_matrix = lgb.Dataset(X_val, label=y_val)

final_model_lgb = lgb.train(params, train_set=train_matrix, valid_sets=valid_matrix,

num_boost_round=13000, verbose_eval=1000, early_stopping_rounds=200)

Training until validation scores don't improve for 200 rounds

[1000] valid_0's auc: 0.731454

[2000] valid_0's auc: 0.733089

Early stopping, best iteration is:

[2303] valid_0's auc: 0.733253

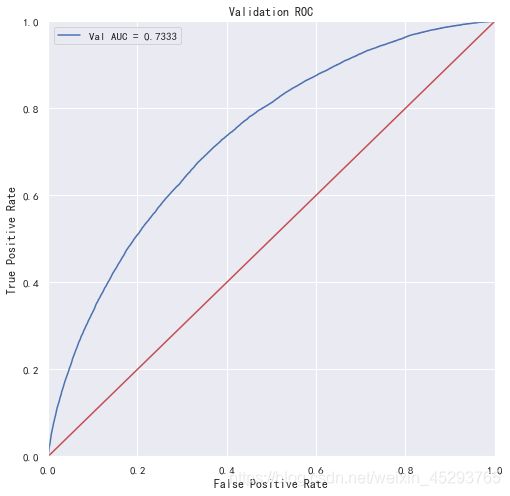

val_pre_lgb = final_model_lgb.predict(X_val)

fpr, tpr, threshold = metrics.roc_curve(y_val, val_pre_lgb)

roc_auc = metrics.auc(fpr, tpr)

print('调参后lightgbm单mox模型在验证集上的AUC:', roc_auc)

plt.figure(figsize=(8, 8))

plt.title('Validation ROC')

plt.plot(fpr, tpr, 'b', label='Val AUC = %.4f' % roc_auc)

plt.ylim(0, 1)

plt.xlim(0, 1)

plt.legend(loc='best')

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.plot([0, 1], [0, 1], 'r-')

plt.show()

调参后lightgbm单mox模型在验证集上的AUC: 0.7332527085057257

相比较原来未调整的参数,模型的性能有所提升。

"保存模型到本地"

import pickle

pickle.dump(final_model_lgb, open('Dataset/model_lgb_best.pkl', 'wb'))